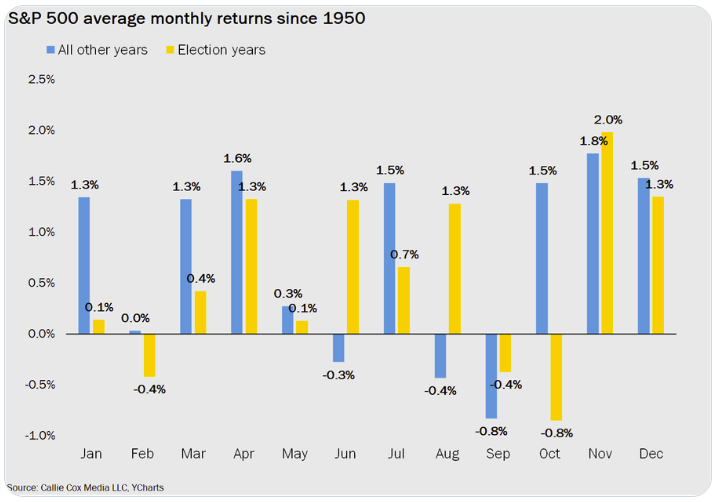

With the U.S. election approaching, the Presidential race is heating up. I wanted to share the chart below, comparing average monthly returns in non-election years (blue bars) with those in election years (yellow bars). While averages provide insights, they don't guarantee similar outcomes every time—just look at September, which ended with a positive return despite historical trends. From an investment perspective, there are no clear rules on how specific election outcomes will affect markets. If you're curious about how election results impact capital markets, U.S. Bank investment strategists analyzed 75 years of data and identified patterns during election cycles. Their findings suggest minimal long-term impact on market performance based on election outcomes. Instead, returns tend to hinge more on economic and inflation trends. Historically, periods of rising economic growth and declining inflation have been linked to market returns that exceed long-term averages. On the other hand, slower growth and rising inflation tend to produce positive, but below-average, returns. For investors, focusing on these economic patterns is likely more insightful for predicting market performance than speculating on election outcomes. Where are we today with macroeconomic data, inflation, fears of recessions, the Fed and interest rates? The economic landscape is currently somewhat uncertain. Despite the Federal Reserve's recent decision to lower interest rates by half a percentage point to address concerns about a weakening job market, the latest employment data has presented a mixed picture. Nonfarm payrolls increased significantly in September, far exceeding expectations. I refer to this uncertainty as "noise." This short-term volatility should not deter us from our long-term financial planning and investment goals. "The best time to invest was 30 years ago. The next best time is now." |