Last week, I encouraged you to consider the core principles guiding your investment decisions and provided a list of questions to help clarify your approach. Today, let's dive into the first question: - Are you focused on short-term gains or long-term growth?

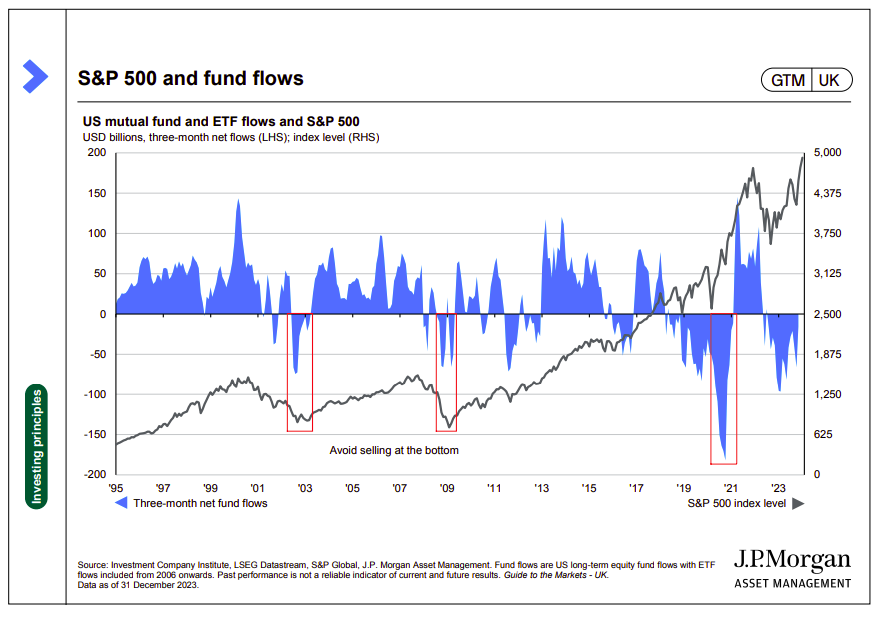

This question is crucial as it defines the type of investor you are—or aspire to be. According to the Corporate Finance Institute, short-term investors typically hold financial instruments for less than one fiscal year, while long-term investors commit to holding assets for more than a year. Now, allow me to be blunt: if your focus is on short-term gains, you're not an investor. Instead, you're engaging in market timing—attempting to predict market movements—or speculating, hoping an asset’s value will quickly increase. This newsletter is dedicated to the principles of long-term investing: why it matters and how to master it. In my humble opinion, backed by over 20 years of studying the markets, advising Ultra High Net Worth Individuals (UHNWI*), and investing myself, true investing is not about "hoping" for a quick profit. Speculation is a risky game, and I strongly advise against it. Why should you avoid market timing? Research and empirical evidence show that timing the market is notoriously difficult and rarely adds value. In fact, it often reduces your chances of achieving your investment goals. As the chart below shows, investors tend to sell after the market has already dropped, locking in their losses and missing out on potential recovery. Advice: Keep your head when others are losing theirs. Last year was a better year for the markets, following a challenging 2022 when U.S. stocks hit lows with a 25% decline. While it may be tempting to sell during such downturns, history suggests that 12 months after a 25% drawdown, returns are often positive. Selling at the market's lowest point is a common mistake that can limit your ability to benefit from the recovery that often follows a downturn. *Ultra High Networth Individuals are private investors with a networth (assets minus liabilities) greater then $30 millions |