Financially literate people can make informed financial choices regarding saving, investing, borrowing, and more. Differently, financial illiteracy carries significant costs, such as consumers who fail to understand the concept of interest compounding, spend more on transaction fees, run up bigger debts, and incur higher interest rates on loans. They also end up borrowing more and saving less money.

Let's start with the correct answers from last week quiz: 1)A; 2)C; 3)B

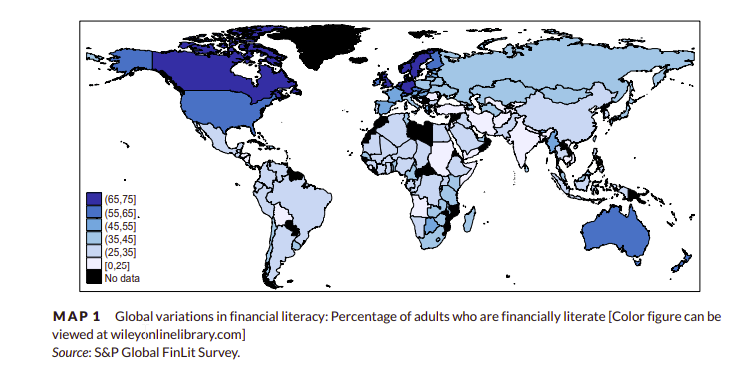

And now, to give you a little bit of context, let's see how financially literate is the world!

Based on the report "Financial Literacy Around the World" (Klapper et al., 2020), only 33% of adults around the world responded correctly to all of three questions and are considered financially literate. The US comes in above the average at 57%. Below some other country's statistics Canada 68% 💥 Italy 37% France 52% Germany 66% 💥 Spain 49% UK 67% 💥 South Africa 42% Mexico 32% India 24% Japan 43% Australia 64% 💥 The least literate countries are Yemen, Albania, and Afghanistan, with literacy rates below 15%. In contrast, Denmark, Sweden, and Norway are the most literate, boasting a literacy rate of 71% (🎉). Unfortunately, women, on average, have lower literacy rates than men. Additionally, both the youngest and oldest adults tend to display lower financial literacy skills. Given that women, on average, have lower literacy rates than men, and that the youngest and oldest adults often struggle with financial literacy, my Instagram page is dedicated to addressing these critical issues. With my extensive background, education, and skills, I aim to empower as many women as possible by raising their financial literacy and, in turn, enhancing the financial knowledge of their children. By sharing everything I know, I hope to create a ripple effect of informed, financially savvy individuals who can confidently navigate their financial futures. |