This is a watchlist composed of the current stocks we are looking to trade none of these are alerts all alerts will be alerted upon entry just like the others on the weekly investment letter.

Company: ATS Corporation

Quote: $ATS

BT: $25- $30

ST: $48

Sharks Opinion:

ATS Corp has been quietly sitting on our watchlist for the last two years. We first started paying attention when EdgePoint a hedge fund we respect and follow closely began consistently increasing their position quarter after quarter. Despite that institutional confidence, the stock itself hasn’t done much during that time, which is partly why we haven’t traded it yet.

But with the robotics theme heating up and investor sentiment starting to shift, we think it’s worth revisiting. In fact, among all the public names in this sector, ATS might be our favorite.

From a fundamentals standpoint, ATS checks all the right boxes: steady revenue, established customers, and manageable debt levels. It’s not some pie-in-the-sky tech promise—it’s a real business with real cash flow.

The stock is thinly traded and sits in the mid-cap range, which likely explains why it hasn’t had its breakout moment yet. That might also present an opportunity.

Second, we see strong M&A potential. Given the increasing importance of robotics across multiple industries and ATS’s positioning in automation, it wouldn’t surprise us if a larger industrial player came knocking. This sector is ripe for consolidation, and ATS has the kind of balance sheet and product depth that could make it an attractive acquisition target.

Lastly and this may sound counterintuitive we actually like that it’s Canadian. Yes, there are plenty of publicly traded duds north of the border, especially in tech and cleantech, but every now and then you find a gem. ATS could be one of those underappreciated names that quietly delivers and gets rerated as the robotics narrative continues to build. Keep it on your radar.

Description: ATS Corporation, together with its subsidiaries, provides automation solutions worldwide. The company is involved in planning, designing, building, commissioning, and servicing automated manufacturing and assembly systems, including automation products and test solutions. It also offers pre-automation services comprising discovery and analysis, concept development, simulation, and total cost of ownership modelling; post-automation services, including training, process optimization, preventative maintenance, emergency and on-call support, spare parts, retooling, retrofits, and equipment relocation; and contract manufacturing services, as well as after sales and services.

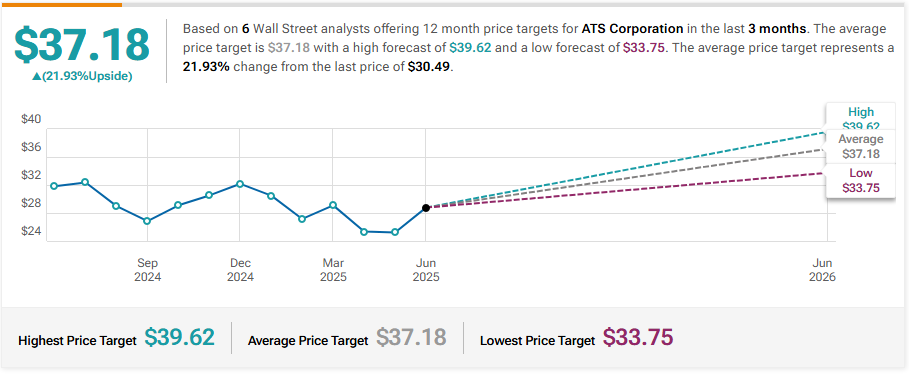

RBC Capital Maintains Outperform on ATS, Lowers Price Target to C$48

Goldman Sachs Maintains Sell on ATS, Lowers Price Target to $30

JP Morgan Maintains Neutral on ATS, Lowers Price Target to $31

Company:Ouster, Inc

Quote: $OUST

BT: Lots of speculation happening right now we want to wait for a big drop off before building a sizeable postion

ST: $28-$30

Sharks Opinion:

Some of our longtime Sharks members might remember Velodyne Lidar one of the more memorable SPAC trades we nailed during the pandemic-era frenzy.

At the time, Lidar was seen as a revolutionary technology, critical to autonomous vehicles and robotic vision. But like many SPACs from that period, Velodyne couldn’t maintain its momentum. As revenues stagnated and investor sentiment collapsed, the company ultimately merged with its competitor Ouster just to survive.

After that merger, we stopped tracking the name closely. Frankly, Lidar felt like a busted theme overhyped, underdelivered, and crowded with too many players chasing too few contracts.

But in 2025, the robotics theme has come roaring back to life, and with it, renewed interest in enabling technologies like Lidar. Ouster (OUST) has been a quiet beneficiary of that momentum. The stock is already up 99% year-to-date, catching a strong wave of capital rotation back into anything related to automation, AI, and advanced sensing.

Now let’s be clear we're not chasing this name blindly. The run-up is significant, and any time a stock doubles in a short window, caution is warranted. That said, just because something’s already moved doesn’t mean it’s finished. If the robotics narrative continues to gain strength, and Ouster can capture even a fraction of that growth, the stock could still have legs.

So while Ouster sits near the bottom of our list in terms of ideal entry timing, it's firmly on our radar again. If we get any kind of meaningful pullback or stronger evidence that large-scale commercial traction is here this could become an actionable setup.

You can read the our full breakdown on Ouster here:

Description: Ouster, Inc. provides lidar sensors for the automotive, industrial, robotics, and smart infrastructure industries in the Americas, the Asia-Pacific, Europe, the Middle East, and Africa. Its products include high-resolution scanning and solid-state digital lidar sensors, analog lidar sensors, and software solutions. The company offers Ouster Sensor, a scanning sensor; and Digital Flash, a solid-state flash sensor.

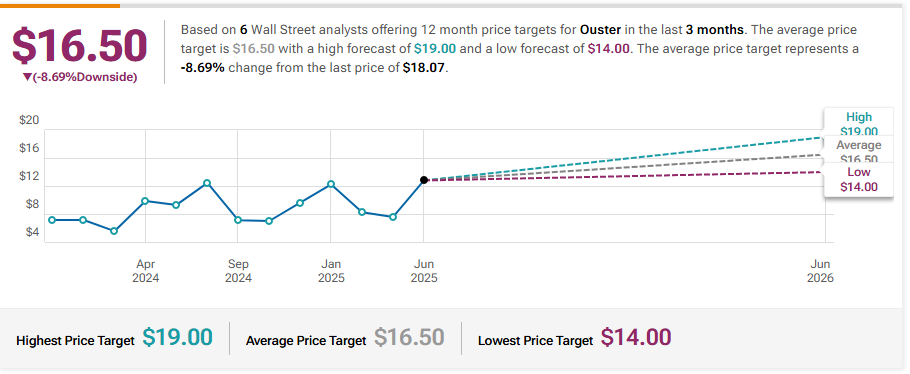

WestPark Capital Upgrades Ouster to Buy, Announces $13.68 Price Target

Oppenheimer Initiates Coverage On Ouster with Outperform Rating, Announces Price Target of $16

Cantor Fitzgerald Maintains Overweight on Ouster, Raises Price Target to $11

Rosenblatt Maintains Buy on Ouster, Maintains $17 Price Target

Company: Xometry, Inc

Quote: $XMTR

Sharks Opinion:

We swing traded Xometry last quarter for a clean win but now it’s back on our radar, and stronger than ever. The stock hasn’t just held its gains it’s pushed higher, with strong volume and solid relative strength. This isn’t a meme pump or a one-off earnings spike. There’s something real building under the hood here.

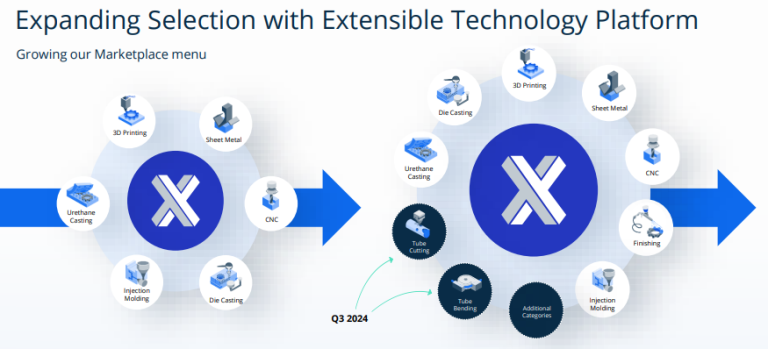

Xometry runs a custom manufacturing marketplace think of it like the Uber of on-demand production. Need precision parts? Xometry uses AI to quote them in seconds, tapping a network of thousands of machine shops to get it made and shipped. In a supply chain world still reeling from post-pandemic inefficiencies, that’s a killer edge.

And in 2025, it aligns with two massive macro themes we’re watching:

AI deployment across real-world industries

M&A tailwinds in fragmented markets

This isn’t just a tech gimmick. The leadership team has serious pedigree. CEO Randy Altschuler sold his first company for $250 million. Co-founder Laurence Zuriff is a hedge fund veteran who now serves as CSO. The two own a combined 15% of the company—meaning their success is tied to shareholder upside. That kind of insider skin in the game? We love to see it.

Here’s the angle: While Wall Street gets distracted chasing flashy tech names, Xometry is quietly becoming a high-leverage AI play on American manufacturing. It’s not just riding hype—it’s booking real orders, adding customers, and scaling intelligently.

Last time we played it, we booked profits. But watching the stock continue to grind higher with conviction and volume tells us the story isn’t over it’s just entering a new phase.

And when that next pullback comes? We’ll be ready. Because XMTR still looks like a high-conviction trade with serious room to run.

BT: $28-$30

ST: $35-$40

Description: Xometry, Inc. operates an artificial intelligence (AI) powered online manufacturing marketplace in the United States and internationally. The company’s marketplace uses AI to assist buyers to source custom-manufactured parts and assemblies and attain instant pricing and lead times. It operates Xometry marketplace, an AI powered online marketplace that connects buyers with suppliers of manufacturing services; Xometry Instant Quoting Engine, which prices transactions based on volume, manufacturing process, material, and location; and Thomasnet, an industrial sourcing platform that features an online directory of industrial suppliers, products, and services, as well as digital marketing services and insights to manufacturers and industrial services providers.

Xometry seeks to reshape the procurement process by centralizing price discovery and shifting transactions online. Rather than manufacturing products itself, it operates as a marketplace connecting buyers with suppliers while dictating the terms of engagement.

At the core of Xometry’s platform lies a trove of proprietary data from millions of past transactions.

This dataset powers an AI model that refines its pricing and lead-time calculations in real-time, incorporating variables such as volume, material, process, and location. A buyer need only upload a CAD file to receive an instant quote—a striking contrast to the slow, manual methods that still dominate the industry.

The value proposition has not gone unnoticed. From SpaceX and Tesla to NASA, BMW, and Amazon, some of the world’s largest companies have embraced Xometry for its efficiency gains.

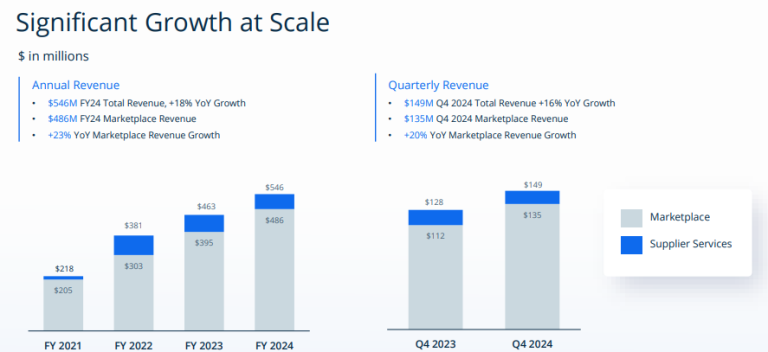

The numbers reinforce the momentum. In Q4, marketplace revenue climbed 20% year-over-year to $135 million. Active buyers increased 23% to 68,267, while the cohort spending over $50,000 annually rose 12% to 1,495.

Not all segments, however, saw growth. Supplier services revenue declined 13% to $14 million as Xometry strategically exited non-core offerings. Meanwhile, the company posted a net loss of $9.9 million—narrowing its deficit by $700,000 from the prior year.

A marketplace that replaces inefficiency with automation is bound to attract attention. If Xometry continues on this trajectory, its role in modern manufacturing could be anything but marginal.

Xometry seeks to reshape the procurement process by centralizing price discovery and shifting transactions online. Rather than manufacturing products itself, it operates as a marketplace connecting buyers with suppliers while dictating the terms of engagement.

At the core of Xometry’s platform lies a trove of proprietary data from millions of past transactions. This dataset powers an AI model that refines its pricing and lead-time calculations in real-time, incorporating variables such as volume, material, process, and location. A buyer need only upload a CAD file to receive an instant quote a striking contrast to the slow, manual methods that still dominate the industry.

The value proposition has not gone unnoticed. From SpaceX and Tesla to NASA, BMW, and Amazon, some of the world’s largest companies have embraced Xometry for its efficiency gains.

The numbers reinforce the momentum. In Q4, marketplace revenue climbed 20% year-over-year to $135 million. Active buyers increased 23% to 68,267, while the cohort spending over $50,000 annually rose 12% to 1,495.

Not all segments, however, saw growth. Supplier services revenue declined 13% to $14 million as Xometry strategically exited non-core offerings. Meanwhile, the company posted a net loss of $9.9 million narrowing its deficit by $700,000 from the prior year.

A marketplace that replaces inefficiency with automation is bound to attract attention. If Xometry continues on this trajectory, its role in modern manufacturing could be anything but marginal.

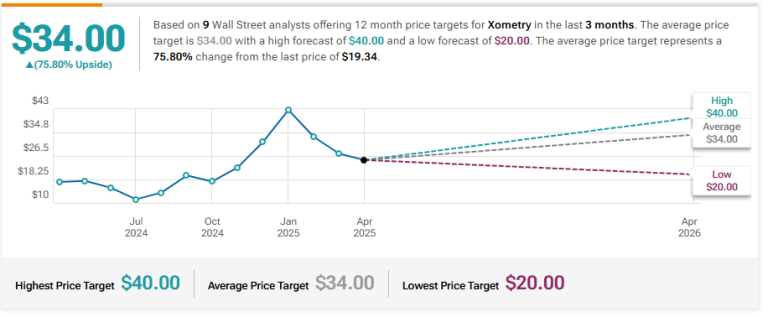

Citigroup Maintains Buy on Xometry, Lowers Price Target to $39

UBS Maintains Neutral on Xometry, Raises Price Target to $33

Cantor Fitzgerald Maintains Underweight on Xometry, Raises Price Target to $20

RBC Capital Maintains Sector Perform on Xometry, Raises Price Target to $40

Company: Starz Entertainment

Quote: $STRZ

BT: $14-$18

ST: $25+

Sharks Opinon:

Let’s be clear: Starz isn’t a sure thing. The entertainment business is a tough place to play low margins, unpredictable cash flow, and heavy competition from tech giants who don’t mind losing money just to win attention.

But here’s where things get interesting.

Starz recently spun off from Lionsgate, and with that came a rare chance to own a pure-play streaming asset outright not bundled with a studio, not tied up in licensing web just the channel itself. And despite operating at a loss, Starz is currently trading below its own revenue, a discount we don’t see often in public markets.

Now we’re not saying this is a core portfolio name. This is a flyer but it’s one with potential.

Since the spinout, insider activity has exploded. Directors, executives, and big holders have been quietly buying up shares on the open market. When the people running the company start putting their own cash in, we take notice. That kind of behavior doesn’t happen unless they see something coming—a strategic move, a shift in fundamentals, or possibly, an eventual buyout.

And that’s the other angle here: M&A.

With legacy streamers bleeding cash and looking to consolidate, Starz could be a target. A bolt-on acquisition for a larger player wanting more niche content and direct subscriber access. Not tomorrow. Not next week. But in this market, media assets at a discount don’t sit idle forever.

We’re watching STRZ closely. It’s not a name you go all in on but it’s one you keep in your back pocket. Because if insider buying continues and the right headlines hit, this one could move fast.

Description: Starz Entertainment Corp. provides subscription video programming to consumers in the United States and Canada. Its business consists of the distribution of STARZ-branded premium subscription video services through over-the-top platforms and distributors on a direct to-consumer basis through the STARZ-branded app and through multichannel video programming distributors. The company is based in Vancouver, Canada.

With its first standalone earnings report post-spinoff, Starz just gave investors a glimpse under the hood and the engine’s got more horsepower than expected.

Let’s break it down:

Q4 revenue came in at $330.6 million, down 6.2% year over year. But here’s the real signal: adjusted OIBDA (Starz’s go-to profit metric) more than doubled—from $45.5M to $93.3M. For the full year, that number hit $201.5 million, just ahead of guidance.

North American subs stood at 19.6 million, with 12.3 million coming from digital. That DTC number is key it’s sticky, higher margin, and gives Starz more control over pricing and churn.

Sure, they haven’t reported EPS yet (first earnings post-separation means no clean net income line), but that’s coming in the Q2 print, and we’ll finally get a real look at the bottom line.

But here’s what we already know: this business is leaner, more focused, and surprisingly cash-efficient.

This isn’t Netflix. It’s not a growth rocket. But for a smaller streaming player operating in a brutal market, Starz is showing the kind of unit economics that turn heads in M&A circles.

With valuation still modest and insiders accumulating, this one’s quietly setting up. Keep your eye on it because if the next report confirms positive EPS and margins stay tight, this could rerate fast.

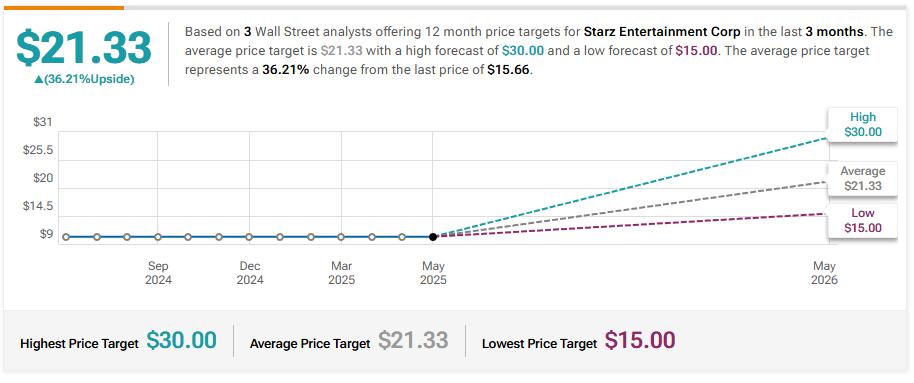

Raymond James Reiterates Outperform on Starz Entertainment, Raises Price Target to $22

Seaport Global Initiates Coverage On Starz Entertainment with Buy Rating, Announces Price Target of $30

This newsletter is sent to you, because you are a customer or subscriber of Stocks

This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.