| Pony AI (PONY)Q1 2025 Earnings Overview

|

Pony.ai reported earnings earlier this week, and its stock has continued to climb, extending a rally that reflects growing investor interest in the autonomous vehicle space.

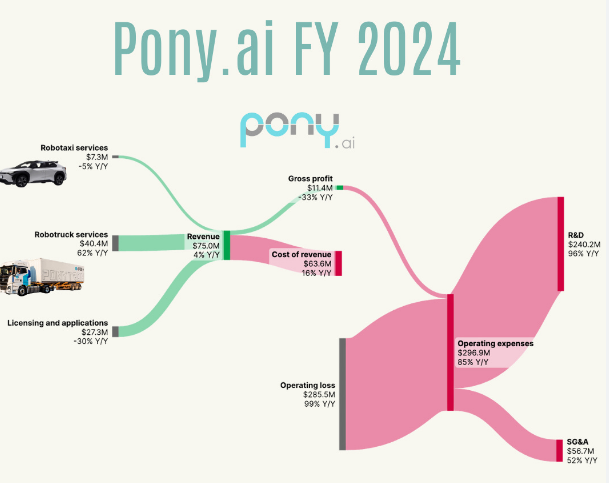

While the company posted a $274 million loss for 2024, management remains focused on scaling production and driving toward profitability by 2026, according to a recent Bloomberg report.

However, that path is not without significant challenges. Regulatory headwinds in China, particularly surrounding recent autonomous driving incidents, present ongoing risks. Additionally, slower-than-expected technology adoption and rising competition across the sector may further delay Pony.ai’s ability to achieve sustainable margins.

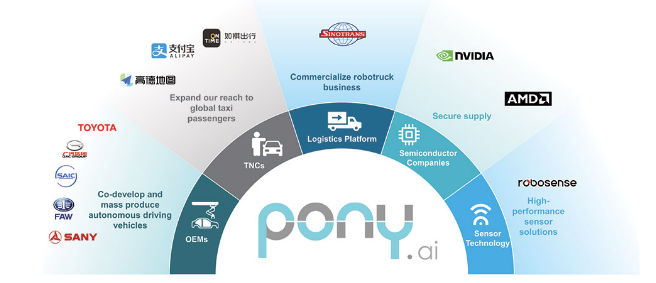

Despite these obstacles, Pony.ai has strengthened its competitive position through a series of high-profile partnerships, most notably with Toyota and now UBER.

This collaboration supported the launch of new robotaxi models at the Shanghai Auto Show, signaling the company's readiness to scale and commercialize its AV technology.

Pony.ai’s growth strategy also includes joint development projects with multiple firms across the autonomous driving ecosystem a move that has helped accelerate product development and expand market reach.

Pony.ai is still in the early stages of commercial development, and profitability remains a medium-term goal. But with a solid network of automotive partners, growing brand visibility, and improving operational discipline, the company is positioning itself as a serious contender in the global autonomous vehicle race.

|  |

Pony.ai has proven to be one of the most volatile positions we’ve ever taken. Upon our initial entry, the stock surged over 35% within three weeks, only to reverse sharply and fall below the $10 mark shortly thereafter.

Most recently, shares have staged a dramatic 300% rebound, pushing the position back into the green a testament to the stock’s unpredictable nature and the intensity of sentiment swings in the autonomous vehicle space.

While we remain confident in Pony.ai’s long-term thesis, particularly given its partnerships, product innovation, and exposure to the growing autonomous driving sector, we acknowledge that the short-term outlook remains highly volatile.

At this stage, the stock’s movement seems driven as much by speculative flows as by fundamentals.

Our current sell target is $28, but given the recent price action, we’re monitoring closely and exercising patience. As of now, it’s clear that anything can happen day to day with PONY, and discipline will be key in managing the trade from here.

|  |

Founded in 2016 by former Baidu executive James Peng, Pony AI has carved a niche not as a traditional automaker, but as a pioneer in fusing advanced robotics with strategic alliances. Chief among these is its close collaboration with Toyota, a partnership that underscores Pony’s ambition to lead in both robotaxis and autonomous freight transport. These alliances, coupled with its technological strides, form the backbone of its competitive advantage.

The Road to Commercial Viability

For all its promise, the true test for Pony AI lies not in innovation alone, but in proving that autonomous driving can be both commercially viable and safe. Investors remain wary of an industry where regulation, liability, and public skepticism loom large. Yet, Pony AI’s rapid expansion in both China and the U.S. two of the world’s most consequential mobility markets—suggests that the company is well-positioned to make a meaningful impact.

Beyond Ride-Hailing: The Freight Ambition

If history has shown anything, it’s that ride-hailing alone is not a golden ticket to profitability. Recognizing this, Pony AI has ventured beyond robotaxis and into autonomous trucking. Recent tests of “truck platooning” where multiple self-driving trucks operate in coordinated convoys—have played out on key Chinese freight corridors linking Beijing, Tianjin, and Hebei Province.

These trials are not mere experiments. With over 45,000 kilometers logged and some 500 TEUs (shipping container units) transported, Pony AI is demonstrating that its technology has real-world applicability. The company’s relentless pace suggests it may be on the verge of a critical breakthrough—one that many have chased but few have captured.

Scaling the Urban Maze

Since its inception, Pony AI has surged ahead of rivals, deploying robotaxis and robotrucks in China’s Tier-1 cities at a pace that has left others scrambling. Yet, as any veteran of the industry knows, self-driving technology is only one piece of the puzzle. Transforming chaotic city streets into structured, navigable grids for autonomous vehicles requires not just sophisticated algorithms, but a deep understanding of regulatory landscapes and market dynamics.

Pony’s vision is not simply to deploy self-driving cars, but to fundamentally reshape urban and freight transport. The question now is whether it can navigate the treacherous intersection of innovation, regulation, and public trust a challenge as formidable as any it faces on the road.

|  |

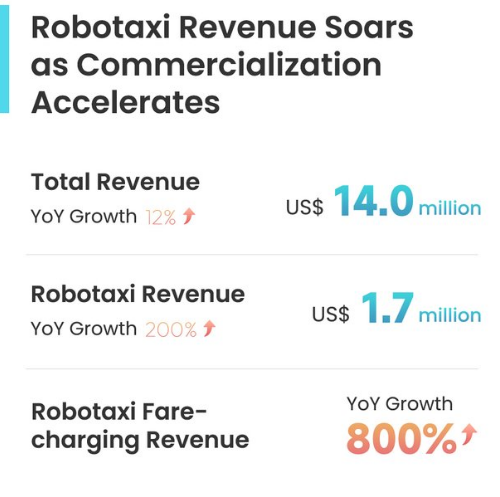

Pony.ai reported total revenues of $14.0 million (RMB 101.6 million) for the first quarter of 2025, representing an 11.6% year-over-year increase from $12.5 million in Q1 2024. The growth was largely driven by continued expansion in Robotaxi services, as the company scales public-facing operations across Tier 1 Chinese cities.

Segment Highlights

Robotaxi Services

Revenue reached $1.7 million, up 200.3% from $0.6 million in Q1 2024. Growth was fueled by both fare-charging and project-based engineering solution revenues, with fare-charging seeing an approximate 800% year-over-year surge. The performance reflects improved geographic coverage and more refined service strategies targeting a broader user base.

Robotruck Services

Revenue came in at $7.8 million, a 4.2% increase from $7.5 million in Q1 2024. Gains were attributed to onboarding new enterprise clients, which contributed to modest top-line growth in the logistics segment.

Licensing and Applications

Revenue held steady at $4.5 million, flat year-over-year. However, orders and deliveries for autonomous domain controllers (ADCs) rose, driven primarily by new robot delivery clients. These hardware sales contributed to overall stability in the segment.

Cost of Revenues and Margins

Cost of revenues rose to $11.7 million (RMB 84.9 million), up 17.9% year-over-year, consistent with revenue growth and operational scaling. Gross profit totaled $2.3 million, down from $2.6 million a year earlier. Gross margin declined to 16.6%, from 21.0% in Q1 2024. The margin compression was primarily attributed to a shift in revenue mix, particularly higher ADC hardware sales at lower margins. The company noted ongoing efforts to stabilize and improve margin performance over time.

Pony.ai continues to show strong growth in its robotaxi segment, underscoring progress toward commercialization. While margin pressures remain a near-term challenge due to product mix, the company’s expanding footprint in both autonomous ride-hailing and logistics — paired with an evolving client base — reinforces the long-term scaling potential of its platform.

| | | | | |

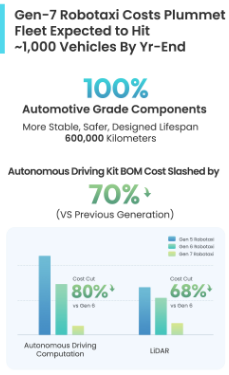

In the first quarter of 2025, Pony.ai significantly increased its investment in research, development, and operational capabilities, reflecting a deliberate push toward mass production and commercialization of its next-generation autonomous vehicle platform . R&D and Operating Expenses Surge Amid Gen 7 Ramp-Up

GAAP R&D expenses rose to $47.5 million (RMB 344.7 million), up 59.8% year-over-year from $29.7 million. Non-GAAP R&D expenses increased to $40.6 million, up 38.1% from $29.4 million in Q1 2024.

The rise in R&D spending was driven by: Investments in mass production capabilities for the Gen 7 robotaxi platform One-time expenses related to IPO-linked share-based compensation Higher employee compensation and benefits to strengthen core technical teams SG&A Costs Reflect IPO-Related and Talent Expansion Efforts

GAAP selling, general, and administrative (SG&A) expenses rose to $10.9 million, a 42.6% increase from $7.6 million in Q1 2024

Non-GAAP SG&A expenses were $8.8 million, up 22.3% year-over-year The increase was attributed to IPO-related share award expenses, higher compliance costs, and expanded compensation across corporate functions.

Operating and Net Losses Widen as Investments Scale

Loss from operations reached $56.0 million, up from $34.7 million in Q1 2024 Non-GAAP operating loss came in at $47.0 million, compared to $33.9 million the previous year

GAAP net loss was $37.4 million, versus $20.8 million in Q1 2024 Non-GAAP net loss totaled $28.4 million, a modest increase from $25.7 million YoY Losses were driven by the same key factors affecting expenses — Gen 7 production readiness, IPO-related compensation, and workforce expansion — and were partially offset by gains in investment income.

Balance Sheet and Cash Flow: Liquidity Remains Strong Despite Heavy Capex

As of March 31, 2025, Pony.ai reported: $738.5 million in cash, cash equivalents, short-term investments, restricted cash, and long-term investment instruments, down from $825.1 million at year-end 2024 The decrease was primarily due to R&D investments, supply chain scaling, and one-time employee-related cash expenses

Cash flow from investing activities reflected this trend: Net cash used in investing activities totaled $93.3 million, compared to $54.3 million in net cash provided in Q1 2024

The swing was attributed to increased purchases of marketable debt securities and long-term investment products, now included in short-term and long-term financial instruments for liquidity management

Bottom Line

Pony.ai’s Q1 financials reflect an aggressive yet deliberate ramp-up toward Gen 7 vehicle commercialization. While losses widened due to scale-up and IPO-related costs, the company maintains a strong cash position and continues to invest in R&D and infrastructure with a view toward long-term market leadership in autonomous mobility.

|  |

Uber announced last week a new strategic partnership with Pony.ai to deploy the China-based autonomous vehicle developer’s robotaxis on its global ride-hailing platform.

The move underscores Uber’s ongoing commitment to expanding its presence in the emerging robotaxi sector, and further validates Pony.ai’s growing relevance in the space.

The collaboration will initially launch in a key Middle Eastern market later this year, with plans to expand into additional international markets over time. The deployment represents a meaningful step for both companies as they look to accelerate the commercial rollout of autonomous ride-hailing services in high-growth regions.

During the pilot phase, Pony.ai’s vehicles will operate with a safety operator onboard, in line with regulatory standards and safety protocols.

The goal is to gradually transition toward fully driverless commercial operations, pending performance validation and local regulatory approvals.

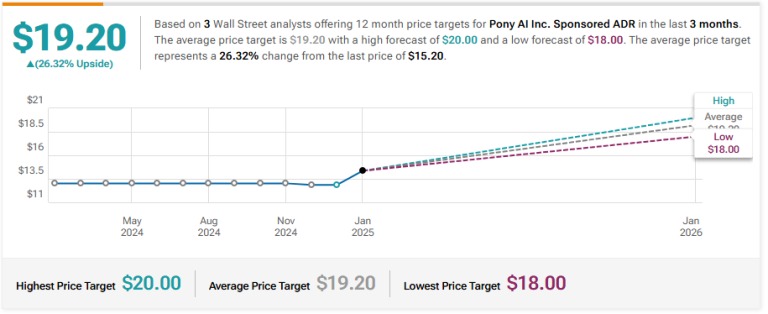

|  | Deutsche Bank Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $20

B of A Securities Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $18

Goldman Sachs Initiates Coverage On Pony AI with Buy Rating, Announces Price Target of $19.6

| | | | | © Copyright, 2025, info@stocksharksresearch.com

This newsletter is sent to you, because you are a customer or subscriber of Stocks | | | This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. | | | | |