|

American Superconductor (AMSC)Q1 2025 Earnings Overview

|

American Superconductor released its fourth-quarter results after the market closed on Wednesday, prompting a 4.2% gain in the stock during after-hours trading. The rally was fueled by stronger-than-expected financial performance, which helped reignite investor interest after a challenging stretch for the stock.

Over the past 3 months, shares of AMSC have fallen 36.3%, sliding to $18.51 then rebounding to $23 prior to the earnings release.

The company has faced persistent selling pressure in recent quarters, weighed down by broader market volatility and sector-specific headwinds. However, the latest earnings report appears to have offered a much-needed reprieve, highlighting signs of operational momentum and potentially laying the groundwork for a near-term rebound.

Investor optimism following the release suggests growing confidence in the company’s fundamentals and long-term prospects. While it's too early to call a definitive trend reversal, the post-earnings price action may indicate a shift in sentiment particularly if the stock can hold or build on these gains in the sessions ahead.

|  |

American Superconductor has staged an impressive recovery, bouncing sharply from its post-earnings pullback and now trading at its highest level since early 2021.

That period marked the height of investor enthusiasm around renewable energy and grid modernization — themes that have returned to the forefront as AMSC regains traction with a more grounded and operationally sound narrative.

While earlier optimism was dampened by concerns over the company’s historical losses, recent developments suggest that sentiment is beginning to shift. Since mid-2023, AMSC has been on a steady upward trajectory, bolstered by improving fundamentals, a more disciplined execution strategy, and renewed institutional interest.

Although the stock did see a brief period of speculative attention during the meme stock surge, its current strength is backed by more durable structural tailwinds, including increased focus on domestic energy infrastructure and electrification technologies.

We’ve named AMSC our preferred “MAGA” pick for 2025 .

Yesterdays earnings report amid broader market uncertainty, further validates the company’s evolving narrative and growth potential. With six-month performance surging and momentum strengthening, institutional eyes are beginning to circle the name more seriously.

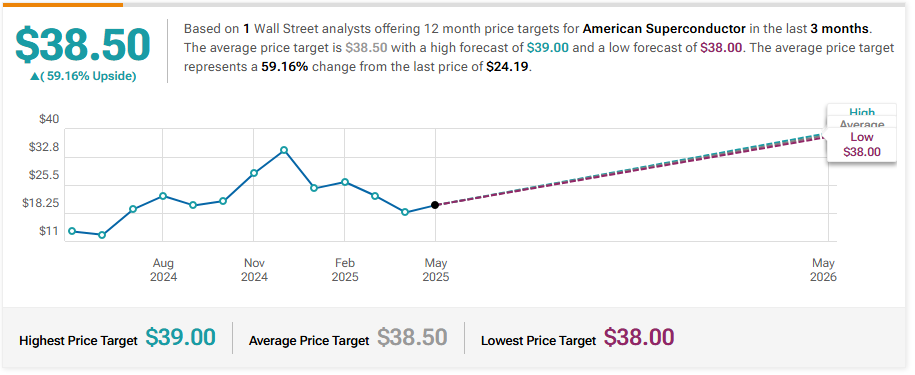

With AMSC we are updating our 2025 price target to $38, reflecting a more bullish stance based on recent volume trends, analyst sentiment, and broader macro alignment.

As always, we’ll continue to monitor the setup for potential consolidation or overbought signals — but at current levels, AMSC remains one of the more compelling U.S. energy tech stories heading into the second half of the year.

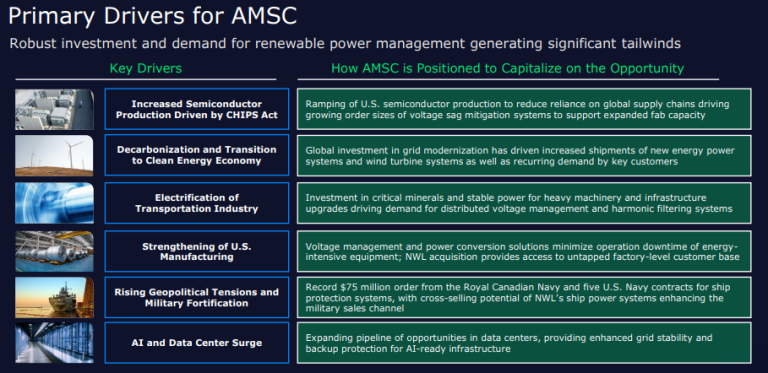

|  | American Superconductor (AMSC) designs and manufactures advanced power systems aimed at modernizing electric grids, enhancing renewable energy integration, and supporting the evolving demands of industrial infrastructure — particularly in sectors like semiconductor manufacturing, where high-efficiency, compact power delivery is essential.

The company’s technologies address the growing need for resilient, scalable energy systems by utilizing high-performance materials and next-generation power electronics that outperform legacy grid infrastructure. AMSC is particularly focused on helping utilities and industrial clients transition to cleaner, smarter energy networks.

Three Core Revenue Streams

AMSC’s business is structured around three distinct but complementary product and service lines:

1. Grid Solutions

At the heart of AMSC’s offering is its Resilient Electric Grid (REG) technology and D-VAR® systems, which stabilize power flows, mitigate voltage instability, and enable the smooth integration of renewable energy sources. These systems are increasingly critical as utilities upgrade aging infrastructure and prepare for a distributed energy future.

2. Wind Energy Solutions

AMSC supplies advanced electrical control systems for wind turbines, empowering manufacturers to improve turbine performance, increase energy output, and reduce maintenance needs. These systems are integral to optimizing wind farm efficiency and long-term profitability.

3. Services and Support

Beyond hardware, AMSC provides comprehensive maintenance, upgrades, and system integration services, ensuring that energy assets operate at peak performance across their lifecycle. This recurring revenue stream strengthens customer relationships and supports long-term adoption.

AMSC’s client base spans utilities, renewable energy developers, and industrial operators, all of whom face mounting pressure to decarbonize, enhance reliability, and scale capacity. Whether integrating solar and wind into the grid, supporting the growth of domestic semiconductor fabs, or safeguarding against blackouts in critical metro areas, AMSC’s solutions are well-aligned with national energy security and clean tech initiatives.

As the global energy landscape continues to evolve, AMSC stands out as a mission-critical enabler of next-generation electric infrastructure — one that is cleaner, smarter, and more resilient.

|  |

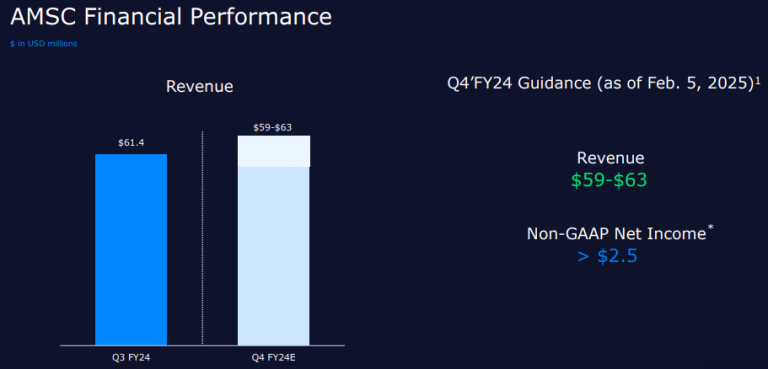

American Superconductor (AMSC) reported a standout fiscal year for 2024, marking a 53% year-over-year increase in revenue to $222.8 million, up from $145.6 million in the prior year. This substantial growth was driven by increased demand for the company’s D-VAR grid stabilization systems, strong performance from NEPSI (New England Power Systems Inc.), and incremental revenue from the strategic acquisition of NWL, Inc.

Just as notable, AMSC swung to positive net income of $6.0 million, a major turnaround from a net loss of $11.1 million in fiscal 2023 — signaling meaningful operating leverage and improved execution across the business.

Q4 Results Exceed Expectations

Quarterly Revenue: $66.7 million, well above analyst estimates of $60.27 million Quarterly EPS: $0.03, in line with expectations Operating Cash Flow (Q4): $6.3 million, supporting financial flexibility Cash Position (as of March 31, 2025): $85.4 million in cash, cash equivalents, and restricted cash These results further affirm AMSC’s ability to scale efficiently while maintaining a conservative capital structure.

Looking beyond this year’s breakout performance, AMSC has quietly delivered impressive compound revenue growth of 26.9% annually over the past five years. This places it well ahead of the average for the broader industrials sector and underscores the durability of its business model and demand for its products.

From grid resilience technologies to renewable integration and industrial power solutions, AMSC’s offerings clearly resonate with a growing base of utility, renewable, and industrial clients.

While fiscal 2024 marked a significant turning point for the company, management remains mindful of potential variability in quarterly operating results and the ongoing need for continued innovation to stay ahead of evolving energy and infrastructure needs. That said, the company's improved profitability profile, strengthened balance sheet, and expanding product suite offer a strong foundation heading into fiscal 2025.

AMSC’s return to profitability, accelerating top-line growth, and long-term sector alignment make it one of the more compelling small-cap names in the energy infrastructure space. With solid fundamentals and strong execution, the company is well-positioned to build on its momentum in the quarters ahead.

|  | American Superconductor’s (NASDAQ: AMSC) recent financial performance highlights the effectiveness of its strategic focus on market expansion and product innovation. The company’s ability to secure $75 million in new orders reflects strong demand across its core offerings and provides a solid foundation for sustained top-line growth in the coming quarters.

In an industry where efficiency, innovation, and scale are paramount, AMSC continues to distinguish itself. The company generated $6.3 million in operating cash flow in Q4, reinforcing its financial discipline and contributing to a healthy balance sheet. As of March 31, 2025, AMSC reported $85.4 million in cash and equivalents, providing ample runway to invest in growth initiatives without near-term liquidity concerns.

AMSC’s focus on expanding its product suite and entering adjacent sectors — including support for semiconductor manufacturing infrastructure and advanced power systems for grid modernization — positions it to capture a broader share of the industrial and clean energy markets. With its proven technology, strong execution, and increasing visibility among institutional investors, AMSC is evolving from a niche player into a formidable name in next-generation energy solutions.

|

| | |  | | Oppenheimer Maintains Outperform on American Superconductor, Raises Price Target to $39

Roth MKM Reiterates Buy on American Superconductor, Maintains $29 Price Target

Craig-Hallum Reiterates Buy on American Superconductor, Maintains $33 Price Target | | | | | | © Copyright, 2025, info@stocksharksresearch.com

This newsletter is sent to you, because you are a customer or subscriber of Stocks | | | This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. | | | | |