| ACM Research (ACMR) Q1 2025 Earnings Overview |

ACM Research reported earnings last week, reaffirming its strong execution and strategic positioning in the global semiconductor equipment market.

The company continues to build on its operational momentum, driven by growing demand for its advanced wafer cleaning and plating technologies.

Notably, ACM delivered another quarter of robust results, marked by continued strength in its core cleaning segment. The company has steadily expanded its market share in China where it now commands more than 25% of the domestic wafer cleaning market translating to over 9% of the global share.

This performance solidifies ACM’s status as one of the top 20 global semiconductor equipment providers in 2024.

Recent tool qualifications with major customers suggest that demand remains resilient and product validation is accelerating. Importantly, management expects minimal impact from current tariff policies, a factor that supports the company’s favorable near-term outlook.

Looking ahead, ACM is guiding for continued top-line and non-GAAP earnings growth, underpinned by strong customer engagement, deepening domestic market penetration, and sustained momentum across its product portfolio.

|  |

ACM Research offers one of the more compelling asymmetries in the semiconductor landscape, a company whose underlying fundamentals are strong, yet whose valuation remains disjointed across jurisdictions.

At the center of this narrative is a striking divergence. While ACM Research (Shanghai), the company's Chinese subsidiary, trades at a valuation of roughly $5.9 billion—or an estimated 6x forward revenue for 2025—its U.S.-listed parent, which owns 82% of that subsidiary, is valued at just $1.54 billion.

With consolidated revenues expected to approach $1 billion this year, the discrepancy suggests a notable arbitrage opportunity. Yet, it's not without caveats.

The strategic risk lies in geography. Over 80% of ACM’s revenue is derived from China, positioning it squarely at the intersection of growing U.S.–China trade and technology tensions.

For investors, this presents a double-edged sword: access to one of the world’s most dynamic semiconductor markets, paired with the constant overhang of geopolitical risk.

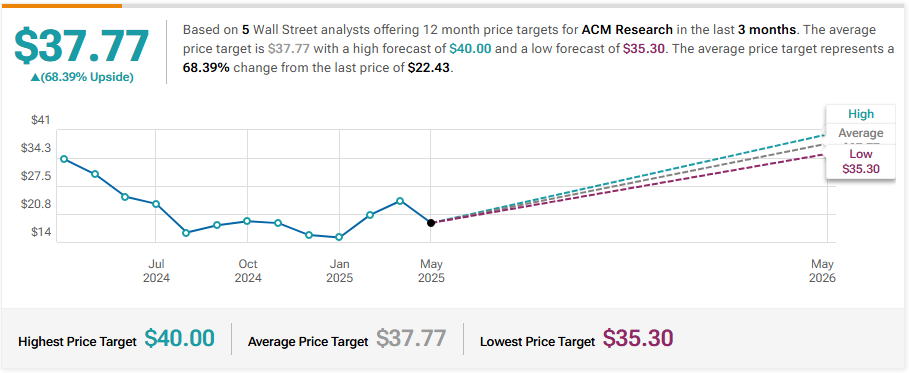

Following its latest earnings, we maintain our $40 price target for the end of the year

|  |

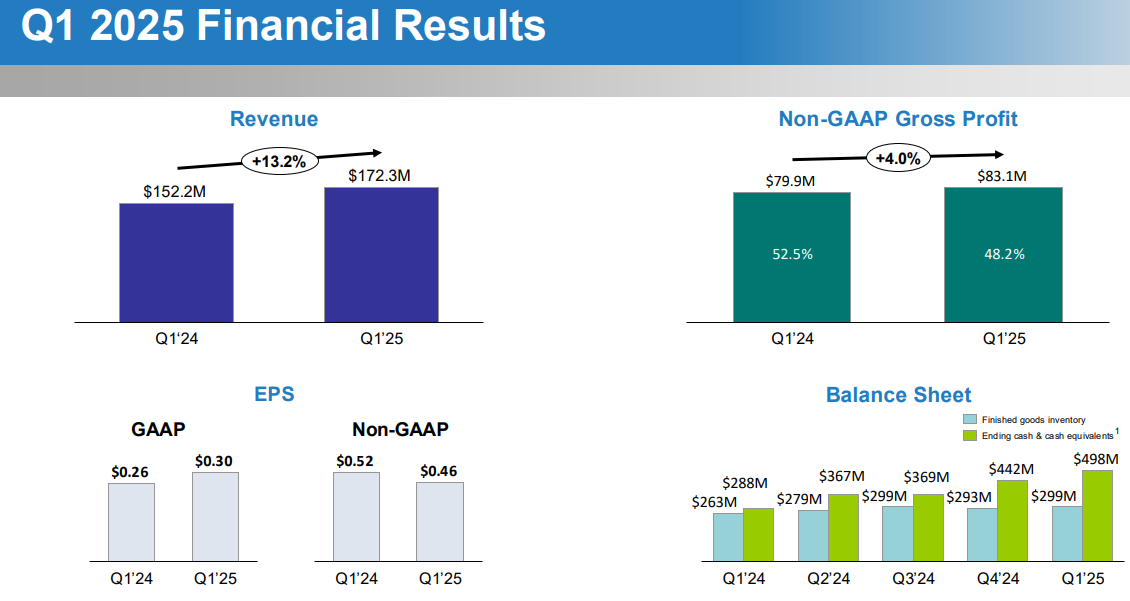

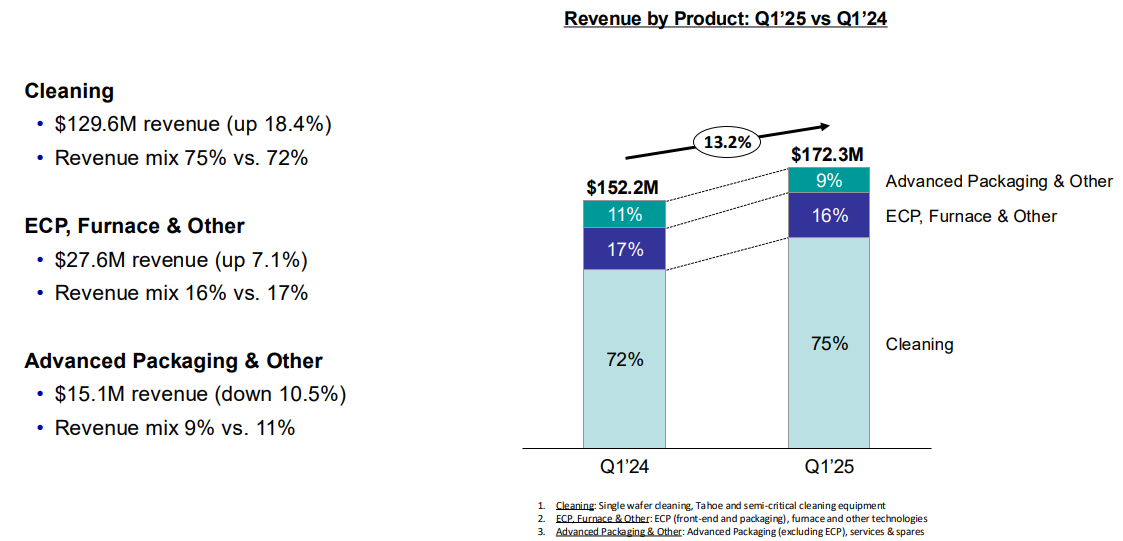

ACM Research reported Q1 revenue of $172.3 million, marking a 13.2% year-over-year increase. This growth was driven by continued demand across its single-wafer cleaning platforms, Tahoe and semi-critical cleaning systems, electrochemical plating (ECP), and advanced furnace and packaging technologies.

Margins and Profitability

Gross margin came in at 47.9%, down from 52.0% a year earlier, though still exceeding the company’s long-term target range of 42% to 48%. On a non-GAAP basis (excluding stock-based compensation), gross margin was 48.2% versus 52.5%. Margin compression was largely attributed to product mix and currency impacts.

Operating expenses rose 5.4% to $56.8 million, but declined as a percentage of revenue to 32.9% from 35.4%, reflecting improved operating leverage. On a non-GAAP basis, operating expenses increased 18.4% to $47.5 million.

Operating income was $25.8 million, up 2.2% year-over-year, representing a margin of 15.0%, down from 16.6%. Non-GAAP operating income declined 10.6% to $35.6 million, with margin at 20.7% (versus 26.2%).

Bottom Line and Balance Sheet

Net income attributable to ACM Research, Inc. rose to $20.4 million, or $0.30 per diluted share, up from $17.4 million, or $0.26, in the prior year. On a non-GAAP basis, net income came in at $31.3 million, or $0.46 per share down from $34.6 million and $0.52 per share, respectively.

Cash and equivalents, including restricted cash and time deposits, totaled $498.4 million at quarter-end, up from $441.9 million as of December 31, 2024, indicating strong liquidity.

Outlook

Management reaffirmed its full-year 2025 revenue guidance, signaling confidence in its long-term strategy and market demand. While near-term margin fluctuations persist, ACM’s market positioning especially in China’s cleaning and packaging spaceremains robust.

|  |

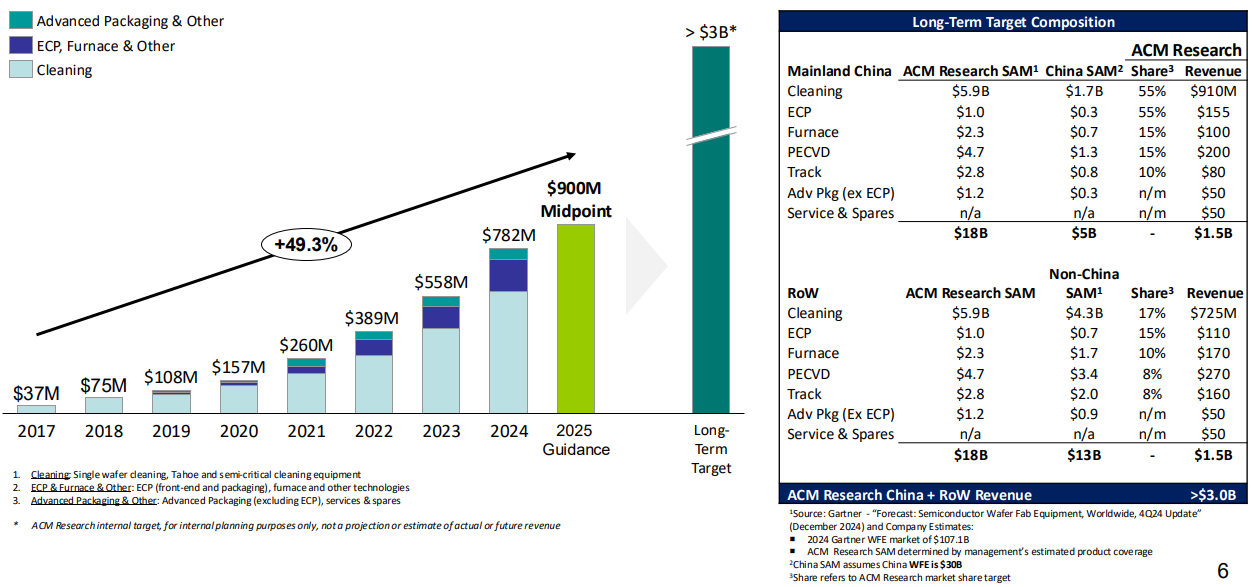

Management reiterated its full-year 2025 revenue guidance in the range of $850 million to $950 million, representing approximately 15% year-over-year growth at the midpoint.

CEO David Wang expressed confidence in shipment volume growth through the remainder of the year, despite the tough comparison to elevated shipment activity in 2024.

He also highlighted upcoming product enhancements namely high-temperature cleaning tools and advanced packaging solutions as pivotal drivers of future expansion and market share gains.

With continued investment in R&D and a clear focus on next-generation semiconductor needs, ACM remains well-positioned to build on its momentum in both domestic and international markets.

|  |

ACM Research reported year-over-year revenue growth of 13.2% in the first quarter of 2025, though sequentially down from Q4’s $223.5 million due to seasonally high shipment volumes in the prior period. Despite the dip, the company maintained a solid growth trajectory and reaffirmed its full-year revenue guidance of $850 million to $950 million.

Gross margin exceeded the long-term target range, reflecting disciplined cost management and a favorable product mix. The company continues to invest aggressively in production capacity and product innovation to meet evolving customer needs in the semiconductor sector.

While analysts flagged concerns around shipment growth sustainability and geopolitical headwinds, management pointed to diversification efforts and strategic positioning as key buffers. The steady guidance and robust pipeline signal confidence in ACM’s ability to navigate short-term volatility while remaining on track for its long-term objectives.

|  |

ACM Research reported total shipments of $157 million in Q1 2025, down from $245 million in the same quarter last year. The decline was partly due to customer pull-ins in Q4 2024, which led to a front-loaded shipment schedule. However, when combining Q4 2024 and Q1 2025, total shipments increased 8.9% year-over-year, suggesting stable underlying demand. Management anticipates a return to year-over-year shipment growth starting in Q2.

On the innovation front, ACM’s single-wafer high-temperature SPM tool was successfully qualified by a major logic chip manufacturer in China. Designed to enhance wet etching and wafer cleaning for sub-28nm nodes, the system reduces acid mist and maintenance requirements, contributing to better uptime and process control. ACM has now delivered SPM tools to 13 customers.

Additionally, the company received the 2025 3D InCites Technology Enablement Award for its Ultra ECP ap-p tool. This copper deposition system—designed for fan-out panel-level packaging—is the first commercially available tool supporting large advanced panels. With its proprietary horizontal plating approach, the tool is expected to solve key challenges in next-generation semiconductor packaging.

|

|  | JP Morgan Initiates Coverage On ACM Research with Overweight Rating, Announces Price Target of $36

Needham Reiterates Hold on ACM Researchto Hold

Craig-Hallum Downgrades ACM Research to Hold, Lowers Price Target to $18

Benchmark Reiterates Buy on ACM Research, Maintains $38 Price Target | | | | | | © Copyright, 2025, info@stocksharksresearch.com

This newsletter is sent to you, because you are a customer or subscriber of Stocks | | | This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. | | | | |