| Schrodinger (SDGR) Q1 Earnings Overview |

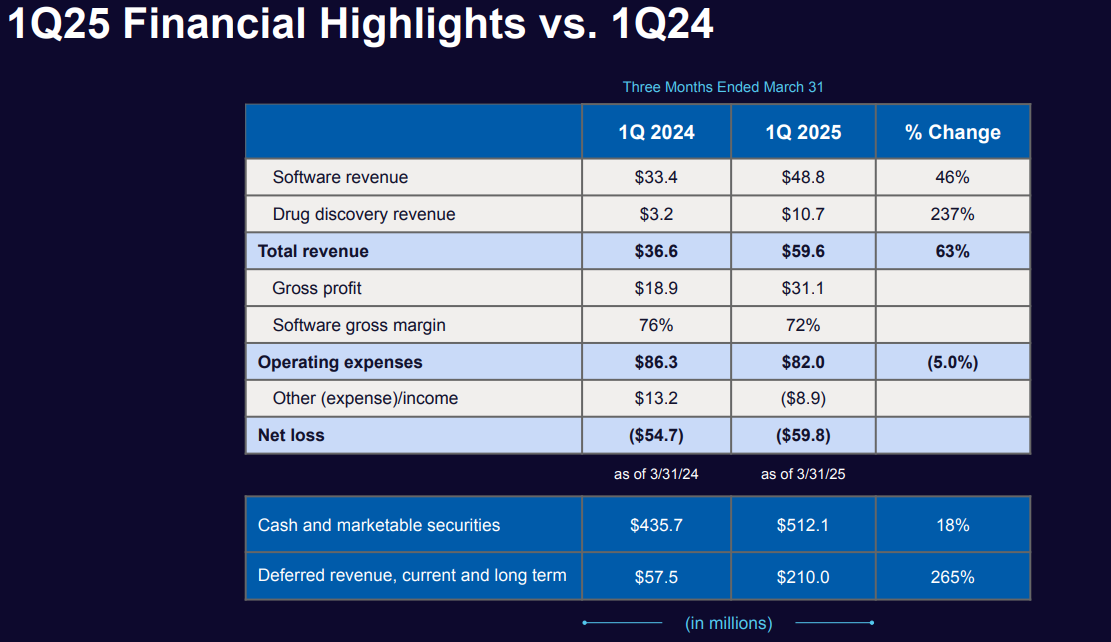

Schrödinger reported first-quarter 2025 revenue of $59.6 million, surpassing Wall Street’s consensus estimate of $54.6 million. The beat was driven by strength across both its software and drug discovery segments, underscoring the company’s growing role at the intersection of computational science and pharmaceutical development.

CEO Dr. Ramy Farid emphasized the increasing adoption of AI-powered modeling and simulation tools in drug discovery and noted that regulatory bodies are beginning to embrace these technologies as part of a more modern approach to clinical development. Importantly, Schrödinger is advancing its proprietary pipeline, with initial data from the Phase 1 trial of SGR-1505 expected next month. This milestone is anticipated to be a key catalyst for the stock and reflects the company’s dual-pronged strategy: combining recurring software revenue with longer-term upside from internally developed therapeutics.

Following the results, shares rose 3.29% in aftermarket trading to close at $24.50, a move that stands in contrast to broader market softness and signals positive investor sentiment around both the earnings beat and continued pipeline momentum. Outlook: With accelerating adoption of its computational platform and a pipeline entering meaningful clinical phases, Schrödinger remains positioned for long-term growth in both software and biotech arenas.

|  |

Schrödinger (SDGR) is a name we’ve followed closely since its IPO, having held it for 2 full quarter.

While the stock has shown brief moments of strength, it has largely remained rangebound, prompting us to reassess our exposure. Unless we see meaningful movement or new institutional interest in the coming weeks—particularly during the ongoing 13F filing season—we’re considering an exit before month’s end.

Our original thesis rested on Schrödinger’s two-pronged model: (1) recurring software revenue from its computational drug discovery platform, and (2) longer-term upside tied to royalties from its pipeline and partnered drug programs. While management continues to guide for substantial royalty-driven value over the next 6–7 years (dependent on the pace of FDA approvals), the software business remains the primary near-term driver of profitability.

That thesis hasn’t broken—but it hasn’t taken off either.

Frankly, we anticipated SDGR would benefit from the AI-driven investment cycle, given its advanced modeling capabilities in pharmaceutical R&D. Yet, despite strong fundamentals and a differentiated model, the stock continues to be overlooked by the broader market, especially relative to other AI-adjacent names.

Context Matters: The healthcare sector was among the weakest performers in 2024, and while a rebound across the group would seem logical, momentum remains elusive. Our Plan: Barring a breakout or unexpected institutional accumulation, we will reassess the position later this month. Our upside marker remains $35, but we are open to reallocating capital if more compelling opportunities emerge.

|  |

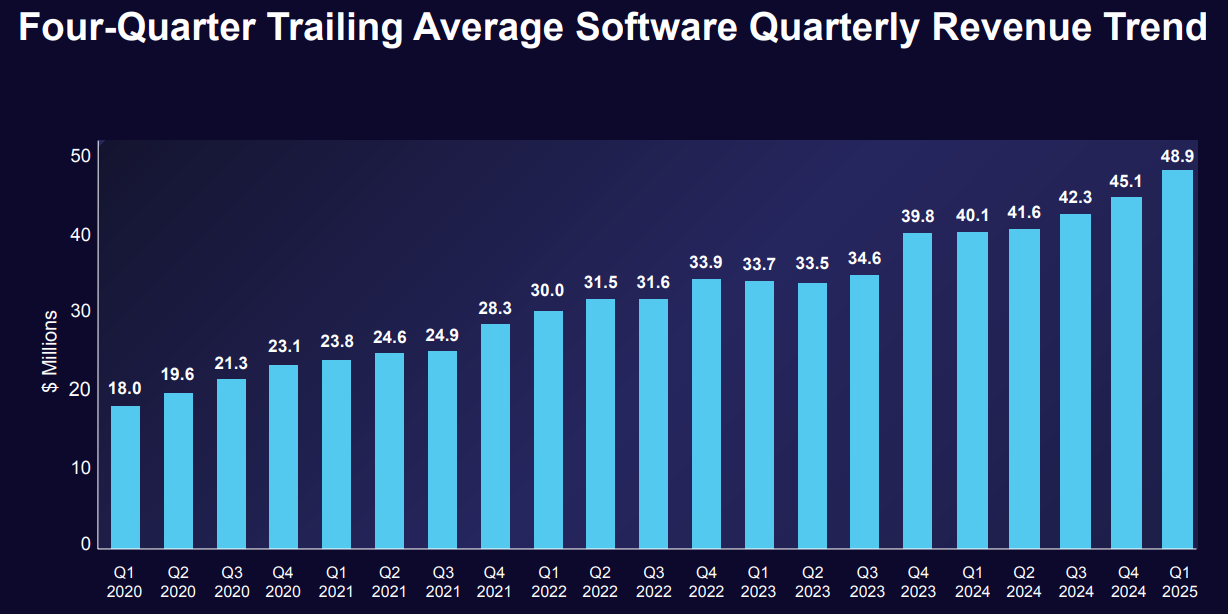

Schrödinger delivered a strong first-quarter performance, with notable year-over-year revenue growth driven by continued strength in both its software and drug discovery segments. The software business was particularly robust, benefitting from early contract renewals with major pharmaceutical clients and growing adoption of computational modeling—a sign that demand for Schrödinger’s predictive technologies is gaining broader traction.

Management reaffirmed full-year 2025 guidance, underscoring their confidence in the company’s growth trajectory despite prevailing macroeconomic uncertainties. A key forward-looking catalyst is the anticipated launch of its predictive toxicology software, which aligns with evolving FDA regulatory focus and may enhance Schrödinger’s positioning within the pharmaceutical R&D ecosystem.

Executive Commentary: CEO Rami Farid noted, “We are having productive discussions with customers and are encouraged about the opportunities for increased adoption of our software.” CFO Jeff Porges added, “We are excited about our approaching clinical data presentations,” signaling potential near-term catalysts from the proprietary pipeline.

Altogether, the quarter reinforced Schrödinger’s dual-growth engine—recurring software revenue and long-term upside from internal and partnered therapeutic programs. If execution remains consistent, the company is well positioned to capture sustained value in the evolving computational drug discovery landscape.

|  |

Schrödinger continues to distinguish itself through an ambitious and synergistic growth model, one that integrates advanced software development with drug discovery partnerships. Rather than passively relying on recurring software revenues, the company has skillfully leveraged its proprietary computational platform to build an internal pipeline and secure high-value collaborations across the biopharma space.

A notable highlight is its stake in Morphic Therapeutics, which is being acquired by Eli Lilly for $48 million. The deal secures both short-term revenue and long-term royalty income for Schrödinger, embedding its platform into Lilly’s development pipeline and reinforcing the company’s strategic role in pharmaceutical R&D.

Unlike many peers navigating costly Phase 3 clinical trials, Schrödinger is focused on an asset-light model: advancing early-stage programs and then partnering or divesting them to major players. This approach not only accelerates monetization but also validates its platform in real-world drug development. Its collaboration roster already includes Bristol Myers Squibb, Sanofi, AstraZeneca, and Bayer, with over ten active programs now advancing through key stages—some approaching IND and Phase 2 trials.

Beyond pharmaceuticals, Schrödinger’s platform has potential applications in materials science, including energy storage, semiconductors, aerospace, and green technologies. Its molecular simulation tools could unlock valuable partnerships in adjacent verticals like battery development, fuel cells, and advanced polymers—industries with massive long-term addressable markets.

With $380 million in cash and no debt, the company maintains substantial financial flexibility. Its ability to self-fund early drug programs while investing in core software improvements gives it an enviable balance of stability and innovation runway. Crucially, Schrödinger’s competitive edge lies in its proprietary database of molecules and AI-accelerated discovery tools, creating high switching costs for customers and a meaningful data moat. While longer-term risks tied to falling computational costs remain, its first-mover advantage and entrenched partnerships provide meaningful insulation.

In sum, Schrödinger is more than just a software firm or biotech play—it is an integrated platform business at the intersection of AI, life sciences, and deep tech. For investors, that combination of recurring revenue, royalty potential, and cross-sector optionality presents a compelling long-term growth thesis.

|  |

Schrödinger reported a strong start to 2025, with first-quarter revenue showing a significant year-over-year increase driven by continued momentum across both its software and drug discovery segments. Notably, software revenue was bolstered by early contract renewals from large pharmaceutical clients and growing interest in the company’s computational modeling capabilities, signaling expanding adoption of its platform across the life sciences industry.

Management reaffirmed full-year 2025 guidance, underscoring confidence in the company’s ability to maintain growth despite broader macroeconomic headwinds. Additionally, the upcoming launch of Schrödinger’s predictive toxicology software is well-timed, aligning with recent FDA initiatives focused on improving drug development efficiency and safety. This new offering could serve as a meaningful catalyst for further adoption and strengthen Schrödinger’s positioning as a critical partner in next-generation R&D infrastructure.

|  |

Schrödinger Q1 2025 Financial Highlights: Strong Growth, Narrower Losses

Total Revenue: $59.6 million, up 63% year-over-year Software Revenue: $48.8 million, reflecting 46% growth Drug Discovery Revenue: $10.7 million Gross Margin: 52% Net Loss: $60 million, or $0.82 per share Cash and Marketable Securities: $512 million

Performance vs. Expectations

Schrödinger delivered a notable earnings beat for Q1. The company reported an EPS of -$0.64, exceeding analyst forecasts of -$0.74. Revenue also came in above expectations at $59.6 million versus the consensus estimate of $54.6 million. These results reflect strong operational execution and growing demand for both Schrödinger’s software solutions and drug discovery services.

|  |

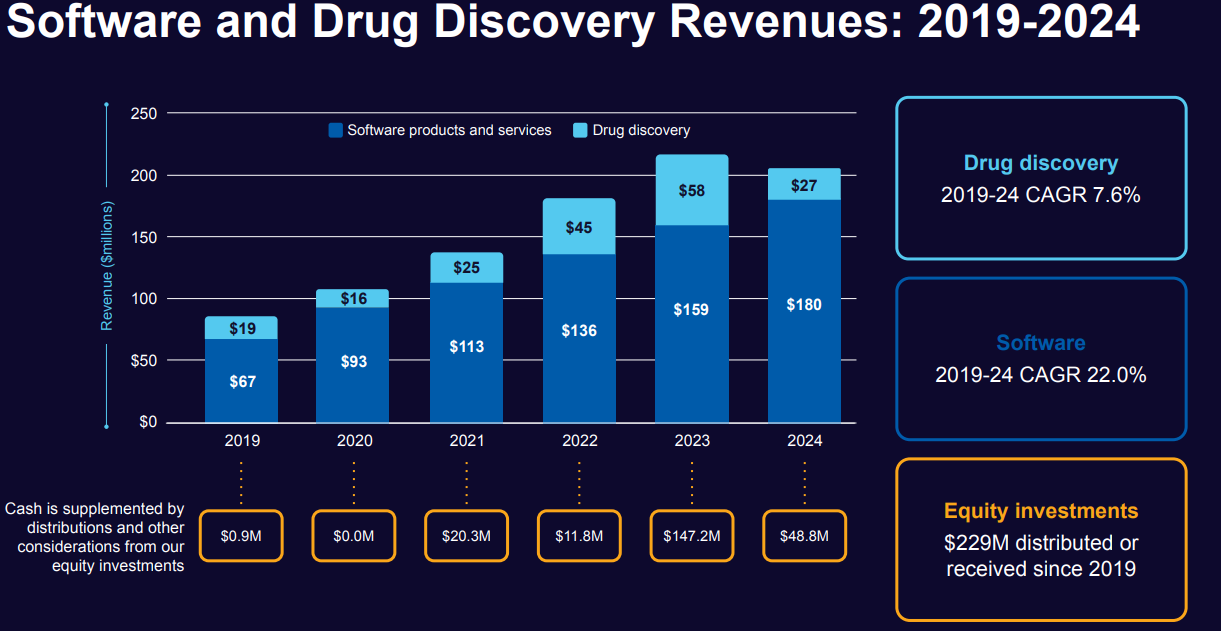

Schrödinger Inc. has continued to distinguish itself as a leader in computational science and software innovation throughout 2024, demonstrating both resilience and a forward-looking approach to growth. Amid a complex drug discovery environment, the company’s expanding software business remains its core engine, anchoring long-term value creation.

One of Schrödinger’s standout achievements this year has been client retention. The company reported a 100% renewal rate on software contracts exceeding $500,000 annually—a rare feat that speaks to the essential nature of its platform within top-tier pharmaceutical R&D pipelines. Notably, the number of clients contributing over $5 million annually has doubled, underscoring growing reliance on Schrödinger’s AI-driven solutions.

While gross margins have come under pressure, this is largely a result of deliberate reinvestment into research and development. A significant portion of these expenditures has gone toward expanding enterprise software partnerships, including deepened collaborations with global leaders like Novartis. These strategic moves are designed to fuel long-term growth and solidify Schrödinger’s position at the intersection of software, life sciences, and AI.

Despite short-term margin headwinds, the company remains focused on building a durable, diversified revenue base—positioned to benefit from structural tailwinds in drug development and computational modeling.

|  | Schrödinger’s Business Model and Flywheel

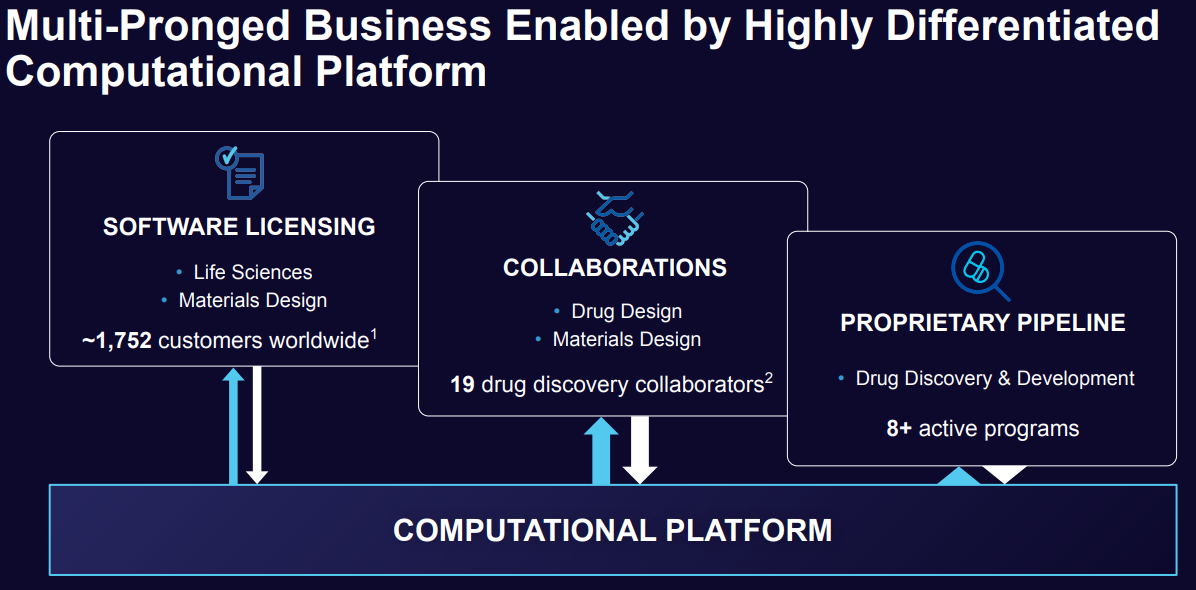

Schrödinger Inc. operates at the intersection of software, drug discovery, and materials science, leveraging its proprietary computational platform to drive innovations across various sectors. The company’s business model is built around a unique combination of software licensing, collaborations, and a proprietary pipeline.

Software Licensing

Schrödinger’s software platform is a core component of its business, offering powerful computational tools for molecular modeling and simulation. The company licenses this software to pharmaceutical and biotechnology companies, as well as academic institutions, enabling users to accelerate their research and development processes. Schrödinger’s software is especially powerful in predicting the behavior of molecules, which aids in drug discovery and the development of novel materials. The platform helps scientists optimize molecular properties, screen large datasets for potential drug candidates, and simulate drug-receptor interactions—all critical steps in speeding up R&D efforts.

Revenue from software licensing forms a steady and recurring income stream, allowing Schrödinger to build long-term relationships with clients. These clients often renew licenses or expand their usage, driving stable growth. Licensing agreements are structured with both upfront payments and ongoing royalties, creating financial sustainability for Schrödinger.

CollaborationsIn addition to licensing its software, Schrödinger actively pursues collaborations with pharmaceutical, biotechnology, and materials science companies. Through these strategic partnerships, Schrödinger is able to co-develop drug candidates and innovative materials, while its partners gain access to the company’s cutting-edge computational platform and research expertise. Notably, Schrödinger partners with leading pharmaceutical firms to apply its technology in accelerating drug discovery, with an emphasis on improving hit identification and enhancing the efficiency of preclinical development.

Proprietary PipelineSchrödinger’s proprietary pipeline represents the company’s most significant value driver. The firm leverages its software platform to discover and develop its own portfolio of drug candidates, focused primarily on oncology and immunology. Schrödinger uses its platform to identify novel small molecules, design drug candidates with improved properties, and advance these candidates through the preclinical and clinical development stages. The company’s pipeline includes several promising candidates, some of which are partnered with major pharmaceutical firms for further development. Schrödinger’s proprietary pipeline creates value in two ways: first, through the potential to generate high returns if its drug candidates are successfully developed and commercialized; and second, through the strategic collaborations that often emerge from its development process, where Schrödinger partners with larger companies in licensing deals or co-development agreements.

Flywheel EffectSchrödinger’s business model operates as a flywheel, wherein each component reinforces and accelerates the others. Software licensing generates predictable revenue, which allows the company to reinvest in its proprietary drug pipeline. Collaborations provide both financial resources and access to expertise, helping Schrödinger refine and develop its pipeline further.

Successful advancements in its pipeline create additional revenue opportunities through licensing or partnership agreements, while also expanding the reach of its software platform to new industries and sectors. This interconnected ecosystem creates a powerful feedback loop: revenue from software licenses supports R&D, which in turn strengthens the proprietary pipeline; collaborations accelerate drug discovery and development, driving more licensing opportunities, and successes in the pipeline generate further partnership interest.

As Schrödinger continues to execute on this flywheel, its capacity to grow its software business and develop proprietary drug candidates positions it for sustainable success in both the technology and life sciences sectors. This integrated approach enables the company to maintain a strong competitive position while capitalizing on the synergies between its technology, collaborations, and in-house drug discovery efforts.

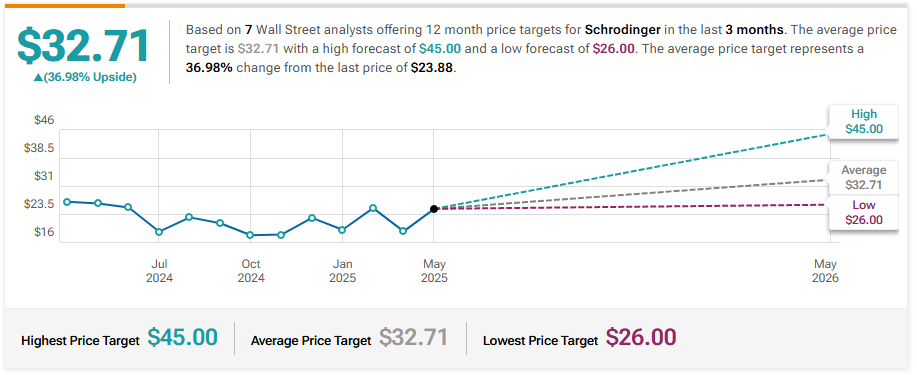

|  | BMO Capital Maintains Outperform on Schrodinger, Raises Price Target to $28

Morgan Stanley Maintains Equal-Weight on Schrodinger, Lowers Price Target to $30

Keybanc Maintains Overweight on Schrodinger, Lowers Price Target to $25

Leerink Partners Initiates Coverage On Schrodinger with Outperform Rating, Announces Price Target of $29

Citigroup Maintains Buy on Schrodinger, Lowers Price Target to $37

Craig-Hallum Maintains Buy on Schrodinger, Lowers Price Target to $30 | | | | | | © Copyright, 2025, info@stocksharksresearch.com

This newsletter is sent to you, because you are a customer or subscriber of Stocks | | | This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. | | | | |