| Plurilock (PLUR,PLCKF) Q1 Update |

Plurilock caught our attention last year as a potential turnaround story, prompting us to accumulate shares around the $0.60 level. Backed by what appeared to be a capable board and a promising cybersecurity narrative, we entered the position with cautious optimism.

Since then, however, the stock has failed to deliver the kind of price action we had anticipated. Performance has remained subdued, and the lack of sustained investor enthusiasm has, for now, tempered our conviction.

That said, the company has made notable operational strides, which deserve attention. Below, we break down the highlights from its most recent earnings report and assess whether the fundamentals are beginning to show signs of life—despite the market’s current indifference.

|  |

Our primary investment thesis for Plurilock hinges on two potential catalysts: a U.S. uplisting and its recently announced strategic partnership with cybersecurity heavyweight CrowdStrike.

A potential uplisting to the Nasdaq would significantly broaden Plurilock’s investor base and increase daily liquidity—benefits the company has not fully realized trading solely on the Canadian exchange. Encouragingly, the company took concrete steps toward this goal in its latest earnings update:

"In its efforts to explore a possible listing or other corporate activities in the U.S., the Company installed new auditors, MNP, to streamline the process of doing an audit under both Canadian (AASB) and U.S. standards (PCAOB)."

The second major development is Plurilock’s partnership with CrowdStrike, which not only strengthens its credibility in the cybersecurity ecosystem but also increases its visibility as a potential acquisition target. In a market where strategic consolidation is accelerating, Plurilock’s positioning becomes more compelling.

Looking ahead, the company expects growing demand for its cybersecurity solutions, driven by the escalating global threat landscape. With improving gross margins and a stated intent to pursue mergers and acquisitions over the next 12 to 24 months, Plurilock may be entering a phase of operational and strategic acceleration—one that, if accompanied by stronger investor recognition, could begin to unlock long-awaited shareholder value.

|  |

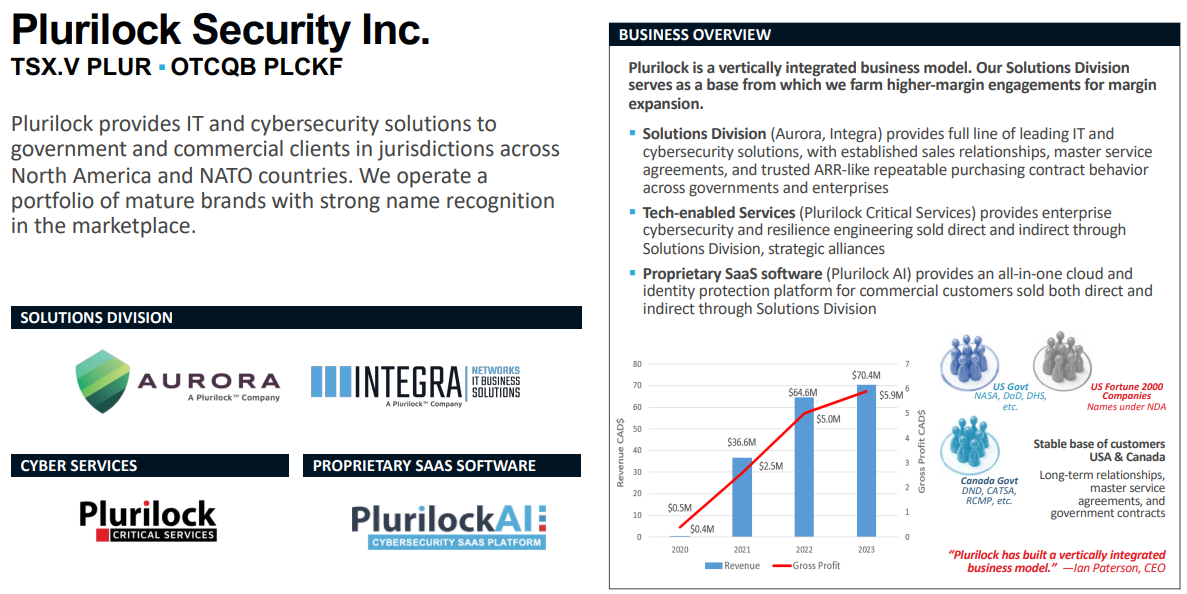

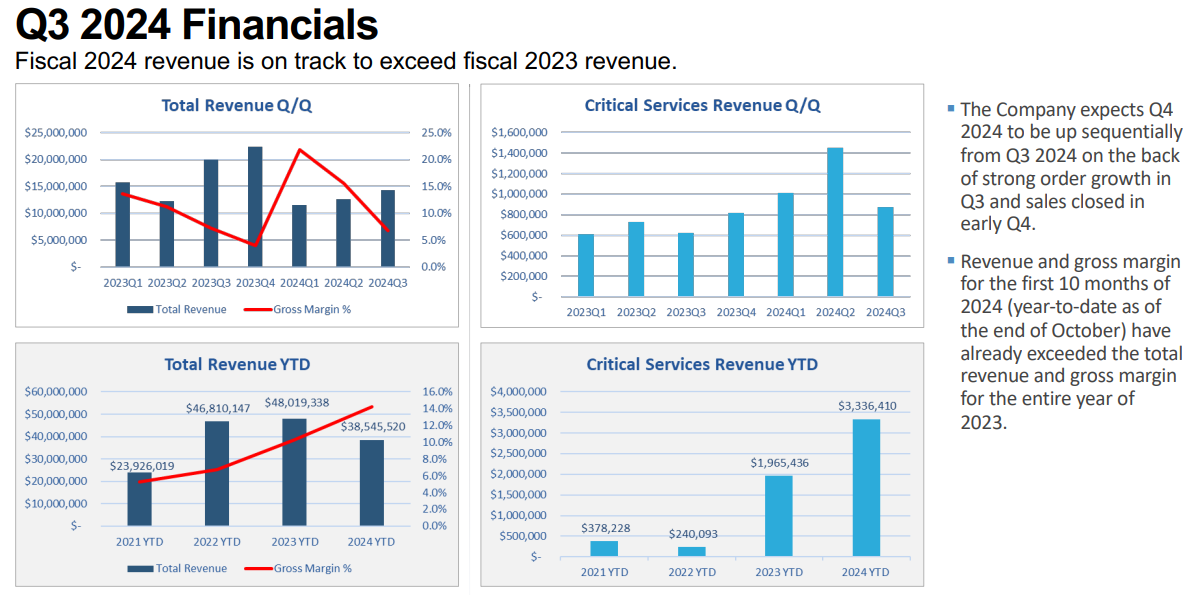

For the fiscal year ended December 31, 2024, Plurilock reported total audited revenue of $59.1 million, essentially flat compared to $59.4 million in 2023.

The modest year-over-year decline was primarily due to the timing of several large orders and a lower volume of re-sell revenue from the Integra (INC) acquisition. These headwinds were partially offset by continued growth in professional services.

Using previous accounting standards, gross sales bookings for the year would have totaled $81.2 million (unaudited), up from $70.4 million in 2023—highlighting underlying demand strength despite reported revenue being flat.

The company’s revenue composition shifted significantly in 2024: Hardware and systems sales accounted for 14.8% of total revenue, down sharply from 31.8% in 2023, reflecting a pivot away from lower-margin hardware.

Software, license, and maintenance revenue increased to 70.5%, up from 62.4% last year—an encouraging sign of Plurilock’s transition toward recurring, higher-margin business lines.

Professional services revenue rose materially, contributing 14.7% of total revenue, up from 5.8% in 2023, driven by increased demand for implementation and consulting services.

Gross margin improved to 13.1%, compared to 8.5% in 2023—a clear sign of better pricing discipline and an improved revenue mix skewing toward software and services.

As Plurilock continues to shift its business toward scalable, recurring revenue, these margin gains suggest the company is progressing in the right direction operationally.

|  | Adjusted EBITDA for the year ended December 31, 2024, came in at $(3.6) million, a modest improvement from $(4.2) million in 2023. The narrowing loss reflects better cost discipline and continued progress toward breakeven operations.

Cash and cash equivalents, including restricted cash, totaled $1.42 million at year-end, compared to $2.06 million in the prior year—a decline driven largely by elevated operational cash use.

The company used $7.1 million in cash from operating activities in 2024, compared to $1.87 million the year prior. The increase in cash burn was due in part to scaling operations and working capital needs amid strategic repositioning.

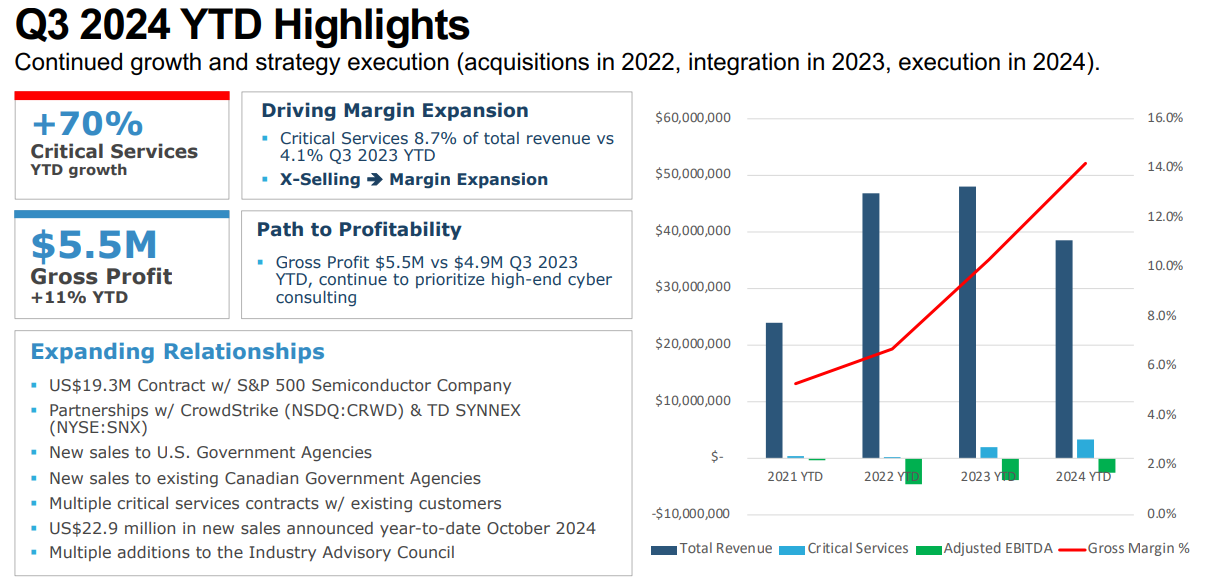

Contracted backlog surged to $56.7 million, more than doubling from $27.1 million at the end of 2023. This sharp increase signals rising demand and forward visibility across Plurilock’s key business lines.

Revenue Mix Breakdown (Audited, FY2024 vs. FY2023): Hardware and systems revenue declined to $8.76 million from $18.87 million, consistent with Plurilock’s strategic pivot away from lower-margin hardware. Software, license, and maintenance revenue rose to $41.69 million, up from $37.08 million, reaffirming the company’s continued shift toward scalable, recurring revenue streams.

Professional services revenue saw a substantial increase, reaching $8.68 million, more than doubling from $3.44 million in the prior year, driven by growing demand for implementation and consulting services.

|  | Plurilock Annual Highlights – FY2024 & Early 2025 Key Milestones in 2024:

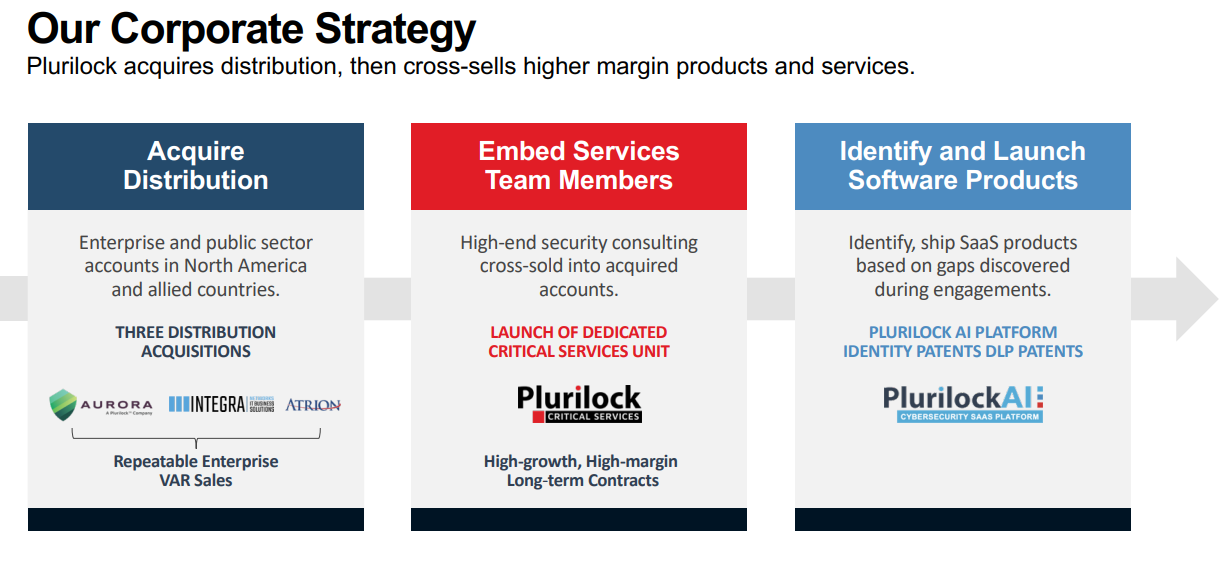

February 21: Launched Critical Services, a new offering aimed at addressing advanced cybersecurity challenges through expert-led consulting and response capabilities.

April 1: Appointed a new Executive Chair and initiated a broad business transformation plan to reposition the company for scalable, strategic growth.

July 9: Expanded engagement with a major S&P 500, NASDAQ-100 semiconductor client under the Critical Services division, reinforcing Plurilock’s presence in mission-critical infrastructure.

August 26: Retained Clear Street to review strategic U.S. listing options and corporate development pathways.

October 3: Secured a landmark US$19.3 million contract with a leading S&P 500 semiconductor company, marking one of the largest wins in company history.

October 10: Formed a strategic partnership with CrowdStrike to enhance security offerings across critical infrastructure and high-risk organizations.

December 11: Received a US$1.1 million order from a Fortune 50 U.S. conglomerate, showcasing rising interest from Tier 1 enterprise clients.

Notable Developments in Early 2025: January 27: Successfully closed an oversubscribed special warrant financing of $4.9 million, strengthening the company’s balance sheet.

February 26: Launched new Offensive Security Services, expanding the Critical Services suite to include proactive threat hunting and red teaming capabilities.

March 25: Announced a partnership with Forcepoint to deliver integrated cybersecurity solutions and broaden access to enterprise markets.

April 2: Announced CAD $5.9 million in new federal and public sector contracts, reinforcing Plurilock’s foothold in government cybersecurity initiatives. |  | | | | | | © Copyright, 2025, info@stocksharksresearch.com

This newsletter is sent to you, because you are a customer or subscriber of Stocks | | | This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. | | | | |