| | Just Do It, Nike (NKE) Deep- Dive 2025

|  |

Nike shares are currently trading at a forward price-to-earnings ratio in the high teens—around 18 to 19 times expected earnings. That’s well below the company’s historical 5- to 10-year average of approximately 30x and near the lowest level seen in the past decade. This compressed valuation suggests the potential for a re-rating if earnings begin to stabilize.

For context, Nike’s current valuation also looks reasonable when compared to peers. Adidas, which is undergoing its own turnaround, trades at around 45x trailing earnings, while premium challenger On Holding commands a much steeper multiple in the 50–55x range.

Even more value-oriented names like Puma and Deckers (the parent of HOKA) trade in the 15–17x range—levels Nike is now approaching, despite its historically stronger brand equity and more robust margins.

In short, the stock is pricing in a lot of pessimism, but that also creates an opportunity if execution improves.

|  |

One of the primary reasons we reinitiated a position in Nike this quarter after reducing exposure last quarter stems from our view that the tariff risk under President Trump’s policies, while headline-grabbing, has yet to materially impact fundamentals.

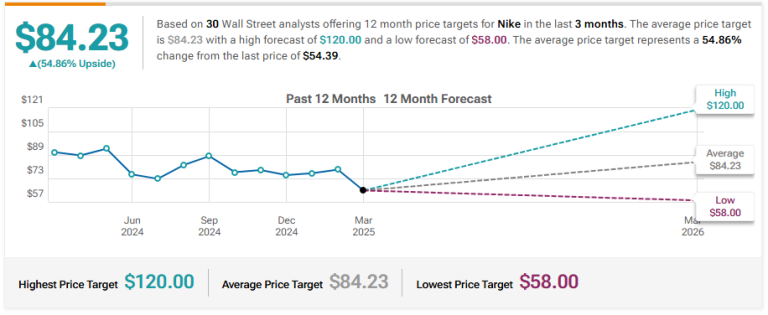

Over the past 100 days, Nike has experienced volatility tied in part to tariff concerns, but the stock has also drawn consistent interest from dip buyers. We entered a position last week, setting a near-term price target of $78 and a longer-term target of $110.

Nike remains one of the most globally recognized consumer brands, but it’s currently working through a challenging transition. Shares are down over 12% year-to-date, marking a third straight year of negative returns. The stock now trades near levels not seen since early 2020, with a market cap below $100 billion and nearly 63% off its late-2021 high.

The near-term pressures are tangible—revenue growth has been soft, margins are under pressure, and the company is still navigating its strategic “Win Now” reset.

However, we remain confident in the brand’s long-term equity.

As macroeconomic conditions stabilize and internal execution improves, Nike has the potential to regain its footing and reward patient investors.

|  | This was Nikes former CEO who messsed up everything. Donahoe, who previously held leadership roles at ServiceNow and eBay, steered Nike toward a digitally focused strategy, emphasizing direct-to-consumer (DTC) sales while pulling back from long-standing wholesale relationships with key partners such as Foot Locker, DSW, Costco, and Amazon. The goal was to enhance margins by consolidating the customer experience.

However, the shift reduced Nike’s in-store footprint at a time when shoppers were returning to brick-and-mortar retail post-pandemic.

This approach misjudged the durability of pandemic-era digital trends. While online sales surged during COVID, many consumers quickly resumed traditional in-store shopping for its immediacy and accessibility. Nike’s decision to limit third-party distribution opened the door for competitors like New Balance, HOKA, ASICS, and Puma to claim shelf space—and market share—particularly in urban and youth-driven retail environments.

Meanwhile, Nike’s innovation pipeline stagnated. The brand leaned heavily on retro silhouettes and color variants of legacy models, such as the Air Force 1 and Dunk, rather than introducing new performance platforms or breakthrough designs. Retail partners increasingly cited a lack of fresh product.

|  | This is Nike’s New CEO The appointment of Elliott Hill as Nike’s CEO, effective October 2024, has brought renewed optimism among investors and analysts. A 32-year company veteran, Hill previously led Nike’s global consumer and marketplace operations and is widely seen as someone deeply aligned with the brand’s heritage, values, and athletic focus. His leadership marks a departure from the tech-oriented strategy of former CEO John Donahoe and reflects a shift back to Nike’s core strengths: innovation, sport, and strong wholesale relationships.

Driving Innovation Forward

Hill has acknowledged that Nike’s product pipeline had stagnated in recent years. Under his direction, the company is investing more heavily in R&D and aiming to accelerate its innovation cycle. New performance footwear platforms are in development for 2025 and beyond, with a particular focus on basketball, running, and training — areas where Nike has historically excelled.

Refocusing Brand Marketing

Nike is also shifting its marketing strategy under Hill. Moving away from celebrity-centric campaigns, the brand is returning to athlete-driven storytelling and sport-centered narratives. Hill has emphasized the importance of local campaigns and integrating marketing efforts with major global sporting events like the Olympics and World Cup. He has spent time reconnecting with athletes, retail partners, and league stakeholders to ensure Nike’s messaging remains authentic and performance-based.

Rebuilding the Retail Ecosystem

One of Hill’s most notable early initiatives has been the rebuilding of Nike’s wholesale partnerships. Acknowledging the overly aggressive pivot to direct-to-consumer (DTC) under the previous leadership, Hill is working to restore relationships with key retail partners such as Foot Locker, JD Sports, and Famous Footwear. The strategy now centers on creating a cohesive retail ecosystem where DTC and wholesale complement one another — supporting brand storytelling, product visibility, and a more premium consumer experience.

Compensation Tied to Performance

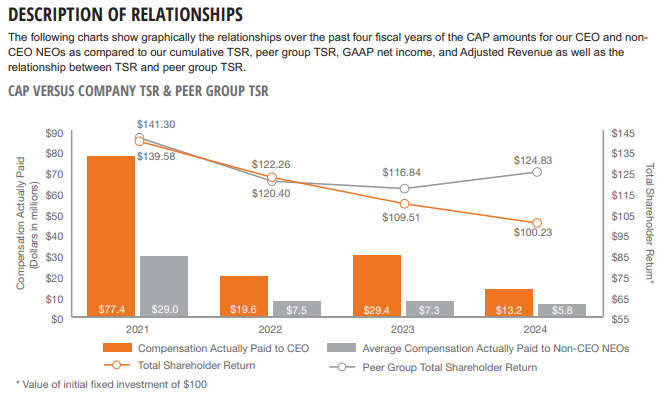

Hill’s compensation package aligns closely with shareholder interests. His contract includes a $1.5 million base salary, a target bonus worth 200% of that base, and long-term equity awards totaling $15.5 million annually — most of which are tied to performance goals and share price appreciation.

Overall, Hill’s leadership appears to be grounded in restoring Nike’s traditional strengths — innovation, sport, and strategic retail execution — while modernizing key functions to meet evolving consumer expectations.

|  |

Earlier this year, Nike entered into a long-term strategic partnership with SKIMS, the shapewear and lifestyle brand co-founded by Kim Kardashian and Jens Grede. The collaboration will introduce a new line, NikeSKIMS, combining Nike’s expertise in sport science and performance technology with SKIMS’ focus on body inclusivity and form-fitting design.

The goal of the partnership is to redefine modern activewear by offering apparel that caters to athletes of all shapes, sizes, and skill levels. The first NikeSKIMS collection is expected to launch in the U.S. later this spring, with a global rollout targeted for 2026.

NikeSKIMS will include a mix of performance-driven apparel, footwear, and accessories that merge technical innovation with a focus on body-conscious fit. The collection is designed to serve both elite athletes and everyday consumers, with an emphasis on comfort, movement, and confidence.

For Nike, the collaboration presents an opportunity to expand its reach in the growing lifestyle and wellness segment while reinforcing its commitment to inclusivity in sport. For SKIMS, the partnership represents a major step into the global activewear market, leveraging Nike’s scale and innovation capabilities to bring a broader product offering to its loyal customer base.

Both companies have described the partnership as a meaningful attempt to blend function and fashion — empowering consumers not only to perform, but to feel strong and supported while doing so.

|  | Nike Inc. is the world’s largest designer, marketer, and distributor of athletic footwear, apparel, and equipment. The company’s portfolio includes the flagship Nike brand—home to globally recognized product lines such as Jordan—as well as the Converse brand.

Nike products are sold worldwide through a mix of direct-to-consumer channels, including Nike-owned retail stores and digital platforms, as well as a broad network of wholesale partners.

The company remains at the forefront of sports innovation, combining performance-driven product development with cultural influence to maintain its position as a leading name in global athleticwear.

|  |

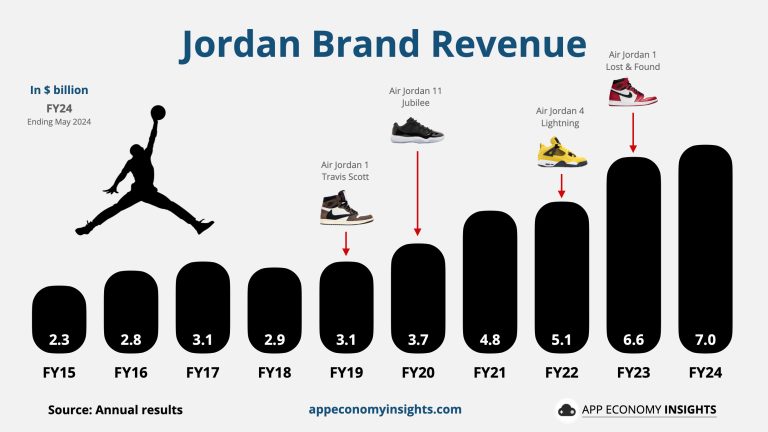

Among Nike’s key divisions, the Jordan Brand stood out as the top performer, delivering 6% year-over-year sales growth to reach $7 billion. In comparison, the Men’s, Women’s, and Kids’ categories posted more modest gains of 1%, 0%, and 1%, respectively.

Since 2020, Jordan Brand revenue has doubled—driven by strategic expansion into women’s apparel, lifestyle offerings beyond basketball, and increased international presence.

While demand for performance basketball shoes has declined over the past decade, the strength of the retro and lifestyle segments has more than offset those losses, underscoring the enduring cultural resonance and commercial success of the Jordan franchise.

|  | Nike, Tariffs, and the Supply Chain Challenge Ahead

Now that we’ve explored Nike’s 2024 missteps under former leadership and the early progress of its strategic reset under new CEO Elliott Hill, it’s worth turning to another major overhang: the Trump administration’s latest round of tariffs and the risk they pose to Nike’s global supply chain.

Nike’s manufacturing footprint, developed over the past three decades, is deeply rooted in Southeast Asia—particularly in Vietnam. The company’s investment in the region has helped transform Vietnam into one of the world’s foremost hubs for footwear and apparel production. But this carefully constructed supply chain now faces serious disruption.

President Trump’s sweeping tariff policy—specifically the newly imposed 46% levy on imports from Vietnam—poses a significant risk to Nike’s cost structure and operational resilience. Vietnam, along with China and Indonesia, accounts for roughly 95% of Nike’s total footwear manufacturing. Together, these three countries employ more than 850,000 workers in Nike’s extended supply chain, a workforce even larger than that of Apple’s main manufacturing partner, Foxconn.

In short, Nike has limited flexibility to pivot production quickly, and any shift in strategy would come with considerable costs and logistical hurdles. Potential options include negotiating with suppliers to absorb part of the tariff burden, increasing operational efficiency, or coordinating with retail partners to pass on some of the added expense to consumers through price hikes.

Despite these pressures, we believe the tariff headwind may ultimately prove temporary. Historically, President Trump has shown a preference for policies that favor large corporate interests, and there are already signs of pushback. This week, the Footwear Distributors and Retailers of America (FDRA) submitted a letter to the White House requesting an exemption from the new tariffs. The letter—signed by 76 companies, including Nike, Adidas, Skechers, and Under Armour—warns that the proposed tariffs pose an “existential threat” to the industry.

For Nike, the next few quarters will test not only its brand strength and innovation pipeline but also its ability to navigate a volatile geopolitical environment. |

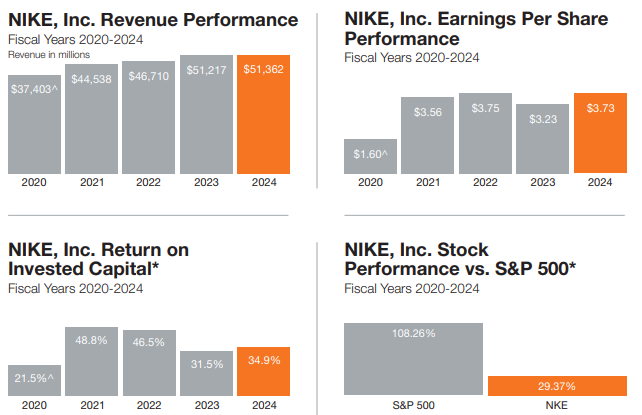

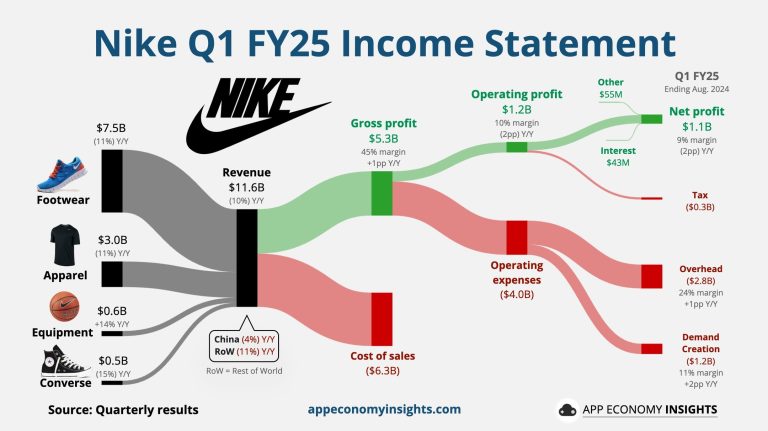

| | | | | |  | Nike’s most recent earnings report felt less like a typical update and more like an acknowledgment of the issues weighing on the business.

Revenue declined 9% year-over-year—marking the fourth consecutive quarter of contraction. Guidance for the current quarter added little comfort, with management projecting a decline near the low end of the mid-teens range.

Margins have also taken a hit. Gross margin dropped to 41.5%, its lowest level in over a decade outside of the COVID period. Management signaled that further margin pressure is expected, which contributed to the stock’s sharp selloff following the company’s March 20 release.

A key issue is inventory. Nike over-indexed on aging product lines that no longer resonate as strongly with consumers. As a result, the company is now clearing excess stock through aggressive discounting and promotional campaigns. While this can help move product, it typically weighs heavily on profitability.

Some of this stems from a strategic decision made during the pandemic. Under former CEO John Donahoe, Nike emphasized its direct-to-consumer (DTC) strategy, scaling back wholesale relationships to prioritize owned retail and digital channels. That move initially paid off as online sales surged, but it became a vulnerability when consumer behavior normalized and shifted back toward multi-brand retail outlets—many of which no longer carried a full assortment of Nike products.

Now, with Elliott Hill back as CEO, Nike is working to course-correct. The new “Win Now” strategy includes rebuilding wholesale relationships, investing in marketing, and refining the product lineup. The goal is to restore Nike’s full-price business and improve margins by aligning supply with more current consumer demand. |  | The causes of Nike’s malaise are manifold. Tariffs and weakening consumer sentiment are the headline culprits, but they mask deeper fractures.

Sales in the third fiscal quarter fell 9%, dragged down by a 17% collapse in China—once Nike’s most promising growth engine.

That retreat reflects not only geopolitical tensions but also the rise of capable domestic competitors and a consumer now less enchanted by Western brands than in decades past.

Closer to home, the backdrop is not especially supportive. Discretionary spending has softened, even as inflation, though no longer surging, remains sticky in services. In such an environment, Nike’s multi-year turnaround effort—centered on product reinvention, innovation, and a rekindling of wholesale partnerships—requires more than just marketing muscle. It needs time, patience, and above all, a consumer willing to pay up for the latest iteration of a legacy brand.

But it is competition, not macroeconomics, that may prove Nike’s most formidable challenge. Once the undisputed ruler of the athletic realm, Nike is now ceding share in core segments to insurgents like On, Hoka, and Lululemon—brands unburdened by legacy systems and fluent in the modern consumer’s vernacular.

| | | | | Geographically, top-line weakness was broad-based. North America revenue fell 8% year over year, driven by a 15% decline in Nike Direct and a 1% drop in wholesale. In EMEA, revenue declined 10%, with a 20% fall in Direct revenue and a 4% decline in wholesale, exacerbated by a strategic pullback in paid promotional activity. Management believes this move will contribute to a more balanced marketplace over time.

China also remained a difficult market. Revenue in the region declined 11%, with Direct down 7% and wholesale down 15%. Retail traffic remained subdued across channels, prompting Nike to increase markdown activity to clear inventory—at the expense of gross margins.

Overall, the results underscore broad-based softness across Nike’s business, driven by both macroeconomic pressures and company-specific challenges. The brand continues to underperform many of its peers as it navigates this period of transition. | | | | | Recent quarters of compressed cash flow have had a measurable impact on Nike’s balance sheet. As of the most recent quarter, the company held $9.8 billion in total cash, short-term investments, and equivalents, against $12 billion in total debt—placing Nike in a net debt position.

Despite this, the company maintains a strong AA- credit rating from S&P Global, reflecting continued confidence in its financial standing.

While the shift to net debt may raise questions, it is not a cause for concern at this stage.

Nike remains financially healthy, with sufficient liquidity and a manageable debt load that provides flexibility to continue investing in the business.

Historically, the company has generated robust free cash flow, ranging between $4 billion and $6 billion annually—more than enough to meet its obligations.

Though free cash flow may remain under pressure in the near term, Nike’s overall financial foundation continues to support its long-term strategic initiatives. | | |  | Piper Sandler Maintains Overweight on Nike, Lowers Price Target to $70

Stifel Maintains Hold on Nike, Lowers Price Target to $64

RBC Capital Maintains Sector Perform on Nike, Lowers Price Target to $66

JP Morgan Maintains Neutral on Nike, Lowers Price Target to $64

UBS Maintains Neutral on Nike, Lowers Price Target to $66 | | | © Copyright, 2025, info@stocksharksresearch.com

This newsletter is sent to you, because you are a customer or subscriber of Stocks | | | This material has been prepared by a sales or trading employee or agent of StockSharks Inc. and is, or is in the nature of, a solicitation. This material is not a research report prepared by StockSharks Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets & Stock market, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that StockSharks Inc. believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. | | | | |